Bank of Japan ends negative interest rates and yield curve control

Can the BoJ claim victory?

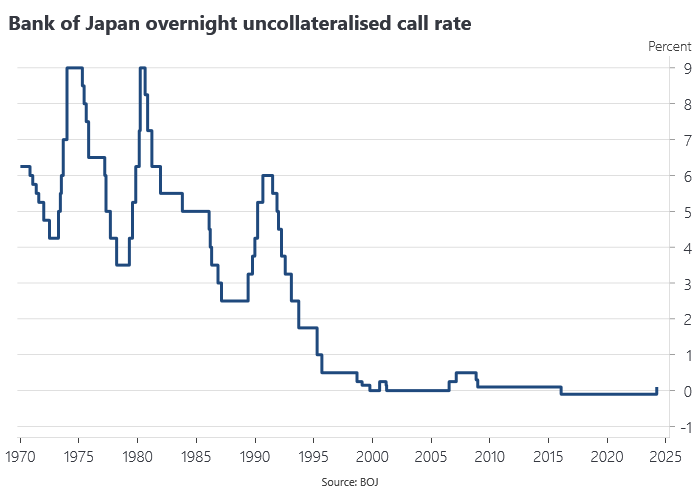

The Bank of Japan raised its policy rate back into positive territory this week at 0-0.1% from the -0.1% rate that had prevailed since 2016. The BoJ will also end its asset purchases in the form of ETFs and J-REITS, as well as commercial paper. Outright purchases of JGBs will continue around current levels, but no longer in support of a reference rate for the 10-year JGB yield.

I have long maintained that the BoJ would end yield curve control and raise its policy rate on its own terms and according to its own timetable. When Governor Ueda assumed office, I argued that his previous record on the policy board pointed to someone who would determine his own path. This is in contrast to some high-profile hedge funds that bet heavily on a forced and disorderly exit on the basis the BoJ could not resist the global trend to higher rates and would be forced to raise its own rates, partly to support JPY.

I have also long maintained that the BoJ’s exit from its now former monetary policy regime would not trigger volatility in global markets. In the event, JPY fell and JGBs declined very modestly in yield in the wake of what was a well telegraphed announcement. Deputy Governor Uchida outlined the BoJ’s exit strategy in a speech in February. The Nikkei once again had the drop a few days out from the policy board meeting. While I am not a fan of central banks leaking to selected media outlets, it no doubt helped smooth any market reaction. Developments in US interest rates will ultimately have a larger impact on US-Japan rate differentials and the associated capital flows.

According to Reuters, the decision to exit the former monetary policy regime was made back in December, leaving open only the question of timing. Perversely, the impetus for the decision came from Japan’s declining inflation rate, with BoJ policymakers concerned that disinflation meant that the exit window was rapidly closing. According to a source quoted by Reuters:

"With the economy lacking momentum, there was a growing feeling within the BOJ that inflation might not stay around 2% that long," said one person familiar with the deliberations, referring to the bank's key target.

"The BOJ leadership probably realised that time was running short, if they wanted to end negative rates."

Assuming the source is accurately conveying the motivation of BoJ policymakers, this suggests the BoJ succumbed to the ‘normalisation’ mantra that demands raising rates for the sake of raising them. The BoJ was looking for an excuse and the strong outcome for the spring wage negotiations was sufficient pretext to pull the trigger on a pre-determined exit strategy.

Japan’s inflation rate is currently above target and the outcome of the spring wage negotiations has left the BoJ more confident that inflation can be sustained around 2%, despite the disinflationary trend in the CPI that leaves the risks to the inflation outlook on the downside.

The BoJ has targeted nominal wages growth of around 3% (2% inflation target, plus a long-run productivity assumption of 1%). Wages per hour worked are currently growing at around 2.5%, which is probably good enough. The BoJ estimates potential output growth is around 1%, with 0.7 percentage points of that coming from total factor productivity growth.

Japan’s negative interest rate and yield curve control regime was viewed as problematic by many, but has largely worked as advertised. As maintained here previously, YCC was the bond market analogue of Lars Svensson’s ‘foolproof way’ of escaping a liquidity trap. Instead of intervening in the foreign exchange market to sell JPY until a price level target was met via imported inflation, the BoJ intervened in the bond market to similar effect. The weakness in JPY, viewed by many market analysts as problematic, was a sign that YCC was working, with the rate differential to the US serving as the main transmission channel. This is all consistent with Sumner’s price of money approach.

Amid a global inflation shock, with other central banks raising their policy rates, there was no better time for Japan to finally realise and even overshoot its inflation target, simply by standing pat. The willingness to back YCC with outright purchases of JGBs when needed ensured there would be no forced or disorderly exit. This is in contrast to the RBA’s experiment with yield curve control, the model for the JGB short-sellers, which very quickly came unstuck when challenged by the market because of the RBA’s reluctance to expand its balance sheet, not because the RBA thought the market was right.

Monetary policy has done much of the heavy lifting in reflating the Japanese economy since 2013, in contrast to the other two arrows of Abenomics, fiscal and structural policy. This was achieved largely be standing pat while the rest of the world experienced a surge in inflation and interest rates, but no less welcome for that. In previous decades, the BoJ would have been all too quick to snatch defeat from the jaws of victory. Despite the perverse motivation for tightening, Ueda gives every indication of wanting to maintain accommodative monetary conditions. The Nikkei has now recovered its ‘bubble’ era highs, at least in nominal terms, although still well short in real terms. Japanese equities have underperformed their US counterparts (no shame in that), but modestly outperformed the world ex-US in USD terms since 2013. That leaves the BoJ sitting on some substantial unrealised gains on its stock ETF purchases. USD-JPY has put in new highs. Based on Sumner’s price of money approach, it is difficult to maintain that there has been a significant effective tightening in monetary conditions based on the BoJ’s announcement this week.

Market monetarists have long contended that extended periods of low interest rates, large QE programs and below-target inflation are a sign of excessively tight monetary policy and monetary policy failure. Since the early 1990s, Japan has been the poster child for the failure to appreciate the importance of monetary policy and its role of determining aggregate demand. The level of nominal GDP is still just below Abe’s now defunct JPY 600 trillion target set in 2015 that was meant to have been reached by 2020.

But recent history shows that Japan has enjoyed better macro outcomes when monetary policy made an effort. While far from perfect, Japanese monetary policy since 2013 has been more successful than it has been given credit for, despite the effort on the part of some hedge funds and others to sell it short.

ICYMI

Trump Economic Advisers Float Three Names for Fed Chair. Kevin Warsh, Kevin Hassett, Arthur Laffer are on shortlist presented to Trump during meeting at Mar-a-Lago.

Auckland’s dwelling stock increased by 15% following planning reforms.

Why Politicians Lie About Trade, a new book by Dmitry Grozoubinski that I look forward to reading.

RBNZ’s LTV restrictions had no significant effect on national house prices.

Doug Irwin’s Richard Snape Lecture on the past and future of globalisation: