Did the 'material miss' just get more material?

Plus, nowcasting Q3 GDP; and prudential controls and the upward filtering of the housing stock

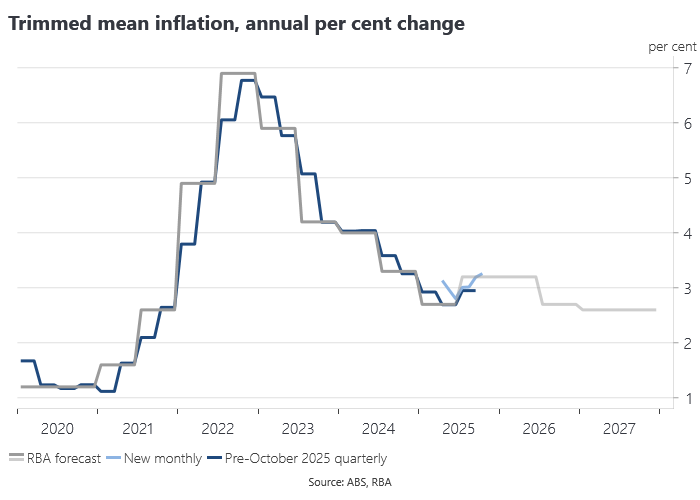

We got the first live release of the new monthly CPI this week referencing the month of October. Inflation surprised on the upside, although at least one institution was looking for an even higher print. Headline inflation was 3.8% at an annual rate, up from 3.2% in the Q3 CPI. Trimmed mean inflation came in at 3.3% compared to 3.2% in September.

With just 16 monthly observations there is not much we can say about the data generating process for the new monthly CPI or its relationship to other variables. The sample mean for the monthly change is 0.3%, if you happen to like super parsimonious specifications. The quarterly CPI will remain the main point of reference for the RBA’s forecasts and monetary policy for some time to come. But at least the transition has started.

Before the release of the Q3 CPI, RBA Governor Bullock set the benchmark for the release by characterising a possible 0.9% q/q print for the trimmed mean as a ‘material miss’ relative to the RBA’s then forecasts. In the event, we got 1%. But neither the headline nor trimmed mean prints for October are significantly out of line with the RBA’s forecasts, which always had inflation rising before falling again in mid-2026.

The RBA views the pick-up in inflation as a number of one-offs, but every CPI print is just an aggregation of largely one-off changes. You can always unpack the CPI and point to temporary influences. It is the underlying data generating process for the overall price level that matters, something the trimmed mean tries to capture. That tells us what inflation is likely to be in future, which is what the RBA should be targeting.

Interest rate smoothing

John Simon had a good piece noting that the RBA is insufficiently activist and suggesting that the RBA’s policy inertia has not changed since the RBA Review. According to John:

The RBA review changed the bank’s governance structure, its communication practices and the wording of its mandate. It changed everything but the one thing that matters: the institution’s appetite for uncomfortable actions.

I don’t think John means that as a criticism of the Review. The Review is best viewed as a necessary but not sufficient condition for seeing improvements in monetary policy strategy and execution.

I have often made the argument that the RBA engages in excessive interest rate smoothing, effectively waiting for the cycle to come to it rather than bringing policy to bear on the cycle. We can see this quantitatively in the interest rate smoothing parameter for the official cash rate (the autoregressive term in the RBA’s reaction function). One the one hand, this is a measure of central bank caution and uncertainty, which is the positive interpretation, but too much smoothing can be symptomatic of the policy inertia that concerns John Simon.

I have also made the point that the cash rate will need to be much more activist now that the Australian dollar exchange rate is no longer carrying as much of the burden of adjustment to shocks. The terms of trade posted record highs in 2022, but you would not know it looking at the exchange rate. Penny Smith argued this week that all the old correlations between international equities and the exchange rate still hold, that we remain a small open commodity exporting economy and that ‘nothing that has occurred in the United States changes that.’ That’s a very dangerous assumption. Those correlations could flip just when you need them most, not least because of what might happen in the US. The cash rate will need to step up in that scenario.

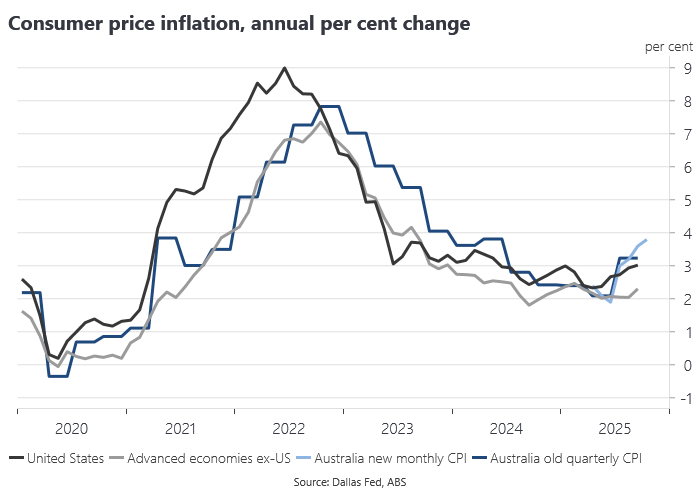

The RBA makes a virtue of Australia’s relative performance, but the inflation rate is notably elevated relative to peer economies.