Disinflation’s progress

The role of housing

The US March CPI came in stronger than expected at 0.4% m/m and 3.5% y/y compared to an annual rate of 3.2% in February. The core CPI (ex-food and energy) came in at 0.4% m/m and a steady 3.8% y/y. The Cleveland Fed’s trimmed mean inflation rate was 0.3% m/m and 3.6% y/y, up from 3.5% y/y previously. The stronger than expected outcome raises concerns about the downward stickiness and persistence of inflationary pressures, implying a higher for longer profile for interest rates. That in turn set-off quite a bit of asset market volatility.

We can still take considerable comfort from the fact that the ex-shelter measure is running at 2.3% y/y, which would still be consistent with the inflation target on a PCE-adjusted basis, notwithstanding the acceleration in ex-shelter inflation since the middle of last year.

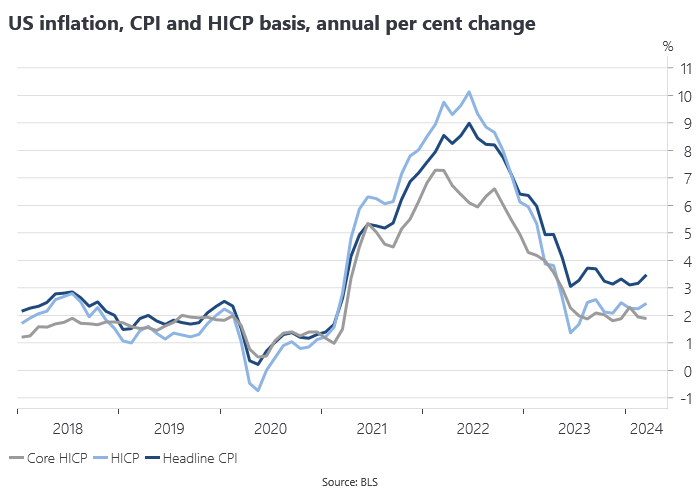

Another way of approaching the role of housing in the US CPI is to put it on the same basis as the EU’s Harmonised Index of Consumer Prices (HICP), which excludes owner-occupied housing. HICP inflation is running at 2.4% y/y and 1.9% y/y on a core basis. The HICP measure shows a similar sideways trend to headline inflation since the middle of last year, but at a lower rate.

The Cleveland Fed’s new tenant repeat rent series actually deflated modestly in the first quarter of 2024 and provides a lead on future all tenant rent inflation, which should provide relief on the headline measure.

Statistical core measures of PCE inflation, the Fed’s target measure, continue to disinflate, albeit lagging headline PCE, so we should be wary of over-interpreting the month to month volatilty in the CPI.

The Fed still looks like it is on top of inflation, but that in itself does not make the case for lower interest rates. The US economy is doing well enough with interest rates where they are and risks of undershooting on the inflation target would seem low relative to the risk of a continued overshoot. If anything the US and world economy show signs of re-acceleration, which is an unlikely backdrop for a major new easing cycle.