It's easy when you're big in Japan

It's easy when you're big in Japan

Is there still life in the JGB short?

With the BoJ scheduled for a two-day policy board meeting on 21-22 September, it is timely to review the Japanese economy and monetary policy.

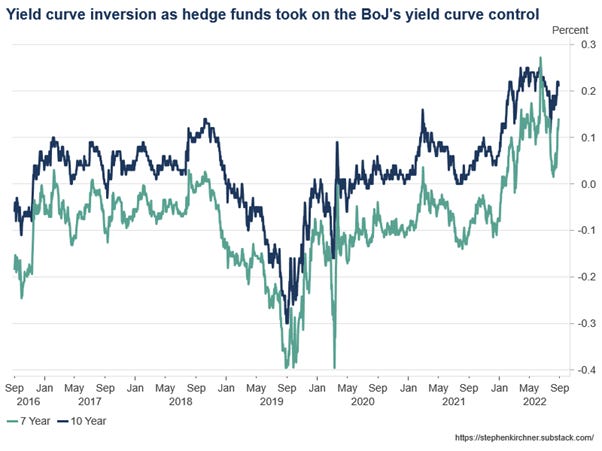

We previously took aim at the BlueBay JGB short and explained why the RBA’s experience with yield curve control was a poor model for thinking about the viability of the BoJ’s 10-year yield target in an environment of rising global interest rates. The short JGB trade can be seen in the following chart of both the 7- and 10-yr JGB since the introduction of the yield target, where the 7-10 yr part of the curve inverts episodically in recent months as funds took a run at the 7-yr as a proxy for the 10-yr. But as the same chart shows, the 10-year didn’t break through the topside of the BoJ’s yield target control range. And while you were all busy shorting JGBs, gilts posted the biggest monthly rise in yields since 1978.

For it’s part, BlueBay had been hanging its hat on the September policy board meeting:

“We have been looking for the Bank of Japan to signal a policy shift in September as inflation continues to rise with the yen trending weaker as policies diverge,” said Mark Dowding, London-based chief investment officer of the $112 billion fund. “This continues to be the case.”

A look at the magnitude of BoJ’s outright purchases of JGBs shows why the JGB short failed. As I argued in my essay earlier in the year, unlike the RBA, the BoJ has no qualms about taking more JGBs on to its balance sheet, whereas the RBA’s yield target was intended as a substitute for balance sheet expansion.

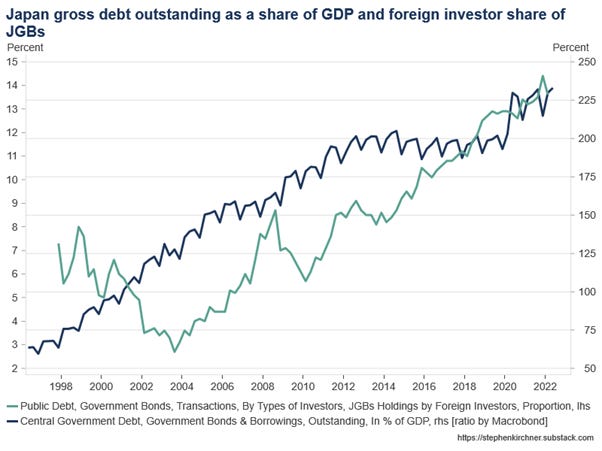

Another long-standing element of the longer-term short JGB thesis is the notion that Japan will trigger a public debt overhang threshold giving rise to a run on its debt. Yet for most of the last 20 years, the foreign investor share of JGBs outstanding has been rising in parallel with the gross debt to GDP ratio:

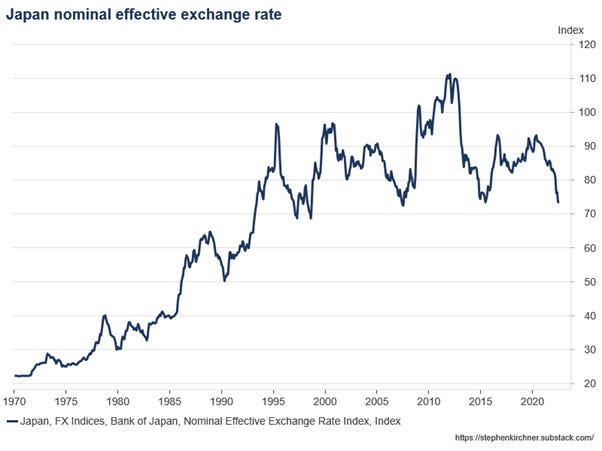

With global yields rising, the BoJ’s yield target has seen Japan’s nominal effective exchange rate to previous cyclical lows, an important contributor to the USD making multi-decade highs. Not that this has stopped the ‘post-dollar world’ op-eds. For the USD doomsday cult, further appreciation is just more reason to be bearish.

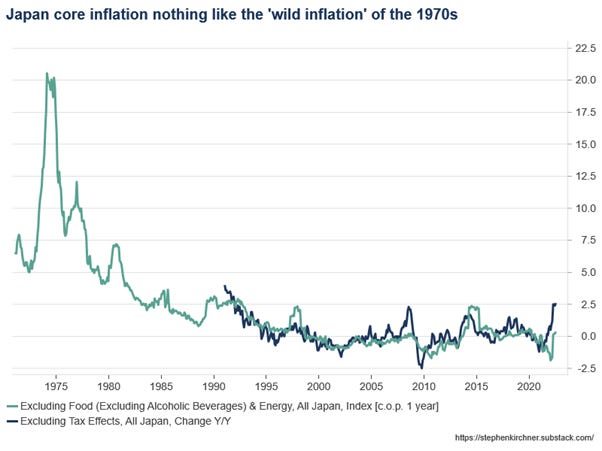

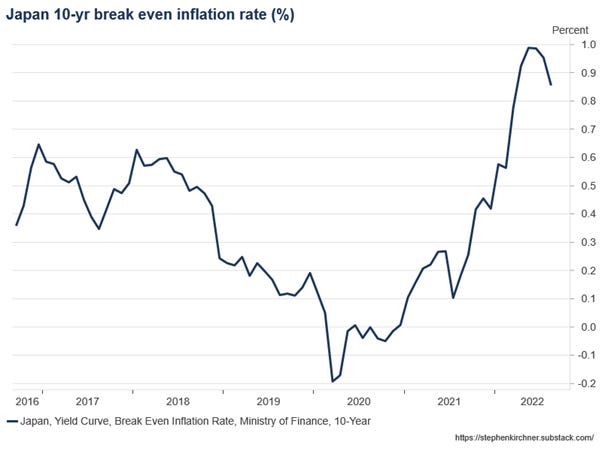

Another element of the short JGBs thesis is that imported inflation pressures due to a weak yen will force the BoJ to let the yield target go. While headline inflation (ex- consumption tax changes) is running at multi-decade highs, core inflation remains barely positive. Compared to the ‘wild inflation’ of the mid-1970s, which is seared into the consciousness of Japanese policymakers much like the Weimar inflation still scars the Germans, the current global inflation shock barely registers. Like much of Asia, Japan is somewhat upstream of global price pressures. The 10-year break-even inflation rate remains below 1%:

In our earlier essay, we suggested that the current environment of rising yields globally is well-suited to implementing Lars Svensson’s ‘fool-proof way’ of escaping a liquidity trap. But instead of pegging the JPY at a level that will meet a price level target, the BoJ has pegged the 10-yr, with similar effect. In principle, this could yield more inflation than the BoJ is comfortable with, but we are not there yet.

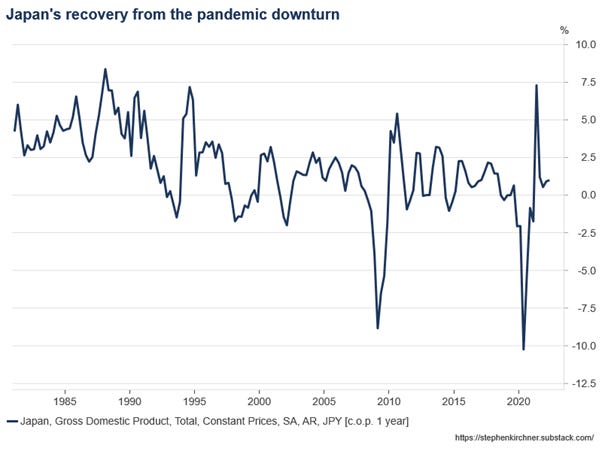

Turning from the nominal to the real and Japan’s real GDP growth rate has normalised around pre-pandemic rates, which is to say, fairly subdued:

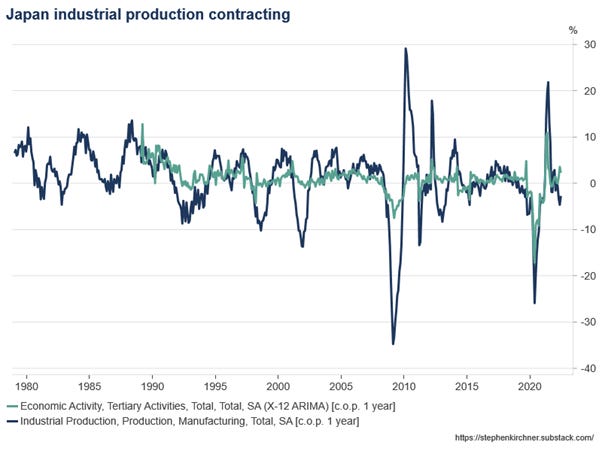

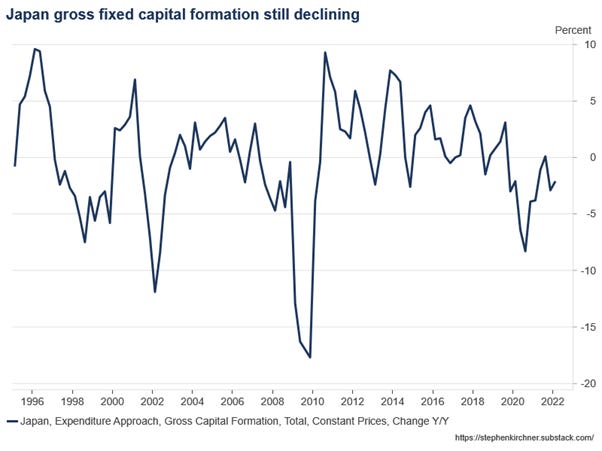

Industrial production is contracting, although the services sector is doing a little better. Capex growth remains negative:

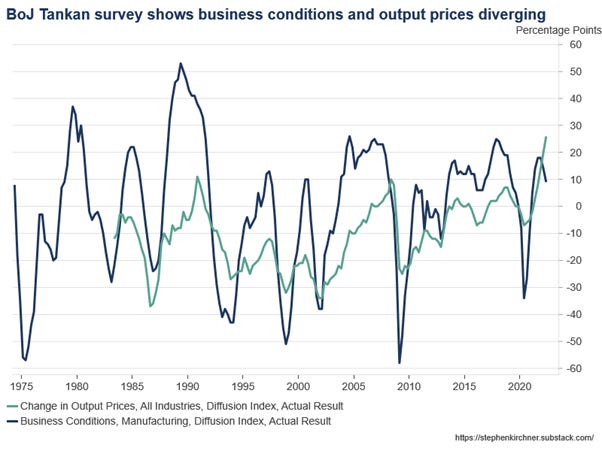

The BoJ’s Tankan survey shows an emerging wedge between business conditions and output prices that is to be expected in the context of supply shocks:

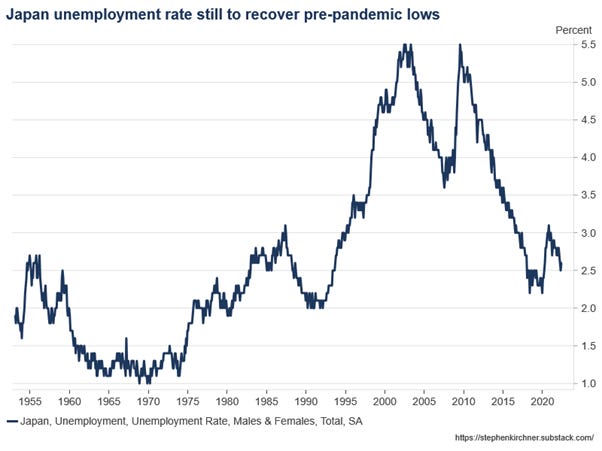

Unlike other economies, the BoJ has yet to recover it’s pre-pandemic lows in the unemployment rate, although the pandemic hit to the unemployment rate was less than a percentage point:

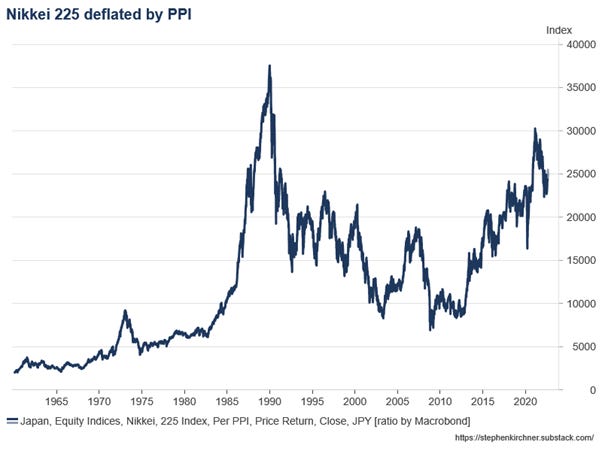

The real Nikkei is often cited as showing no gains to a buy and hold over the last 30 years, but this ignores significant cyclical variation along the way. Time the cycle right and you made money. But more notable is the uptrend since the introduction of Abenomics, for which monetary policy did most of the heavy lifting:

Governor Kuroda’s term expires on 8 April 2023 and the remainder of his term will define his legacy. With the Governorship likely to revert back to a BoJ insider with stronger anti-inflationary preferences, the next eight months represents perhaps the best chance for Japan to consolidate the reflationary gains from Abenomics.

ICYMI

FRED has produced a handy dashboard of indicators referenced by the NBER’s Business Cycle Dating Committee for identifying peaks and troughs in the business cycle.

PGIM white paper on DM stock-bond correlations, including Australia.

Monetary policy shocks may have bigger effects when interest rates are low.

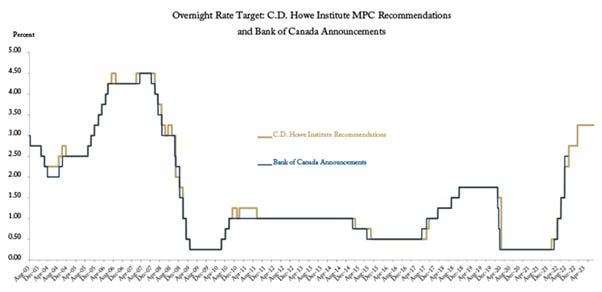

C.D. Howe Institute’s Monetary Policy Council (MPC) recommends that the Bank of Canada raise its target for the overnight rate, its benchmark policy interest rate, by 75 basis points to 3.25 percent on September 7th, and maintain the current pace of reduction in its holdings of Government of Canada bonds. Worth noting the MPC’s mostly hawkish policy bias:

Yield Curve Control and Zero Interest Rate Policy in a Small Open Economy: Why price level targeting is superior to yield curve control.

The failure of the Big Aussie Short (and supply-side housing policy) in one chart:

Meme stocks: