Japanese markets after the BoJ

Japanese equities join JGBs as the new widow maker

Bloomberg was not happy with the Nikkei getting the drop on BoJ policy board decisions, calling for a parliamentary inquiry into the leaks, which is fair enough from their perspective. But when it comes to being wrong-footed by Japanese monetary policy, the media have nothing on financial markets. This ultimately has more to do with misplaced market narratives than the BoJ’s actions.

The new 34-years highs in USD-JPY have left the yen the worst performer against the USD this year and sparked a lot of head scratching on the part of those who expected last week’s BoJ decision to catalyse a major shift in global capital flows. Taken in isolation, it was not unreasonable to expect a change in at least the notional policy stance by the BoJ to be more supportive of JPY. But we saw much the same reaction in response to previous tweaks in the former yield control framework, which induced similar levels of head scratching at the time. The weakness in JPY and the decline in JGB yields should lead us to question whether the effective stance of policy has significantly tightened.

The unexpected weakness in JPY is partly a USD story. The US economy has proven more resilient than expected and this has supported USD-JPY and the yen carry trade. The US-Japan 10-year yield differential remains at levels last seen on a sustained basis in the late 1990s and early 2000s. If you want to make a case for major reversal in USD-JPY, you need to make a case for a significant narrowing in the rate differential as a necessary, if not sufficient, condition. That is more likely to come from the US rather than the Japanese side of the spread, but not yet.

Japanese equities have joined JGBs in becoming something of a widow maker, at least for the long-short equity hedge funds that have long viewed Japan as a chronically mean-reverting market and traded it accordingly. The poster child for secular stagnation has massively outperformed China, the secular growth story, now turned sour.

The prospects for FX intervention

The new lows in JPY have seen the MoF again threatening intervention in the fx market. The MoF intervened heavily in September and October 2022, but has been quieter since. The MoF’s historical intervention profile suggests it is more tolerant of JPY weakness than strength. A strong yen offends the MoF’s mercantilist desire for export-led growth and it is the MoF rather than BoJ that makes the intervention decision. The MoF is typically less concerned about the inflationary implications of JPY weakness, although the post-pandemic run-up in inflation is politically unpopular. In 2003-04, the MoF was intervening so heavily to curb JPY strength it was all but fully financing the current account imbalance with the US and the rest of the world.

Reflation dynamics and monetary policy

The failure of Japanese markets to cooperate with the expected post-monetary tightening script once again comes down to misperceptions of the effective stance of policy. Japanese monetary policy has long been viewed as ‘ultra-easy,’ despite macro outcomes that argued the opposite. Prospective changes in the notional stance of monetary policy, such as tweaks to the former yield curve control range, have been given too much weight as a potential driver of markets.

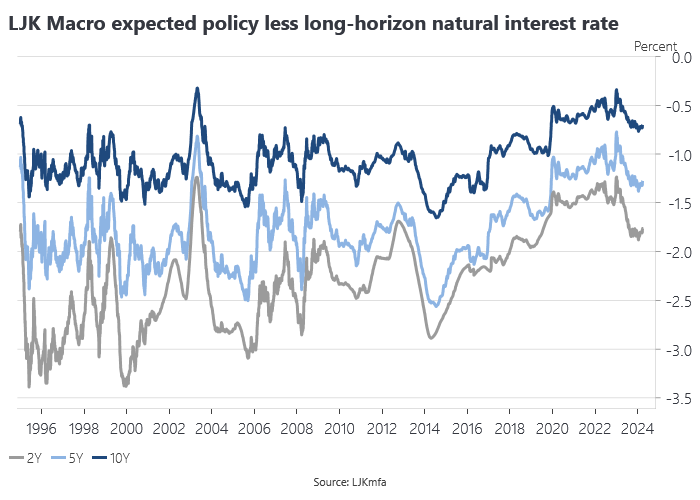

Measures of the long-horizon neutral interest rate have been rising more recently along with estimates of potential output, meaning that the effective stance of monetary policy has if anything eased rather than tightened, at least based on the LJK Macro Finance estimates. Note how the early years of Abenomics drove the estimate of the neutral rate to around 3%, which is more or less where it should be given a 2% inflation target and 1% potenial output growth. The five-year moving average of nominal GDP growth, a proxy for expected NGDP growth, is now back above potential output growth.

LJK Macro produce estimates of the difference between policy rates based on the forward rate curve and its estimates of the long-horizon natural rate. These imply that the effective stance of monetary policy has eased more recently, but that’s largely a function of a rising natural rate rather than the policy rate. This speaks to the market monetarist point that the neutral rate is not independent of monetary policy, which complicates the interpretation of New Keynesian/macro finance-based interest rate gaps, even if we can agree on the neutral rate. The reflation of the Japanese economy has likely raised the equilibrium interest rate, making Japanese monetary policy seemingly more stimulatory for a given policy rate.

Measures of the central tendency of inflation, which capture the persistent component predictive of future inflation, have been declining since September last year and are now broadly target-consistent. The 10-year break-even inflation rate has been rising but remains below the BoJ’s 2% target, suggesting market-based inflation expectations remain anchored, notwithstanding the usual caveats about the quality of price formation in that market.

When it comes to inflation, the BoJ is not standing on a burning platform. The adjustment to policy had more to do with taking advantage of favourable conditions to change its monetary policy operating framework than effecting a meaningful tightening in monetary conditions. This interpretation is far more consistent with the price action in JPY asset markets since the BoJ adjusted it framework.

Those looking to the BoJ to rationalise bearishness about Japan will need to look elsewhere. For now, Japan has the distinct benefit of not being China at a time when China’s growth model is failing. As the Rhodium group noted this week, China’s growing trade surplus is a sign of a deeply troubled economy at risk of sparking a global protectionist backlash not unlike that seen by Japan in the 1980s. ‘Japanification’ is not just about the demographics, but also the dangers of state-led industrial policy.

ICYMI

The city that declared all-out war on landlords – and what happened next.

Zoning reform in Auckland: what can we learn from the literature?

The Resolution Foundation’s damning look at UK housing. Australia not far behind.

Trend-Cycle Decomposition After COVID. The BN filter seems to handle the COVID shock well. See also this handy online tool to implement the KMW modified BN filter using FRED.

China’s Economic Collision Course. As Growth Slows, Beijing’s Moves Are Drawing a Global Backlash.