Markets and the US Presidential election

Plus, the China stimulus that nearly wasn’t; and the Australian Q3 inflation outlook

With the US Presidential election now only a few weeks away, prediction markets are getting more attention. The FT had a nice story profiling Kalshi’s court victory over the CFTC. Kalshi now facilitates institutional bets on the election outcome of up to USD 100 million and bets of USD 12 million were placed in the first few days. As one political scientist is quoted as saying:

You may want more institutional money because while these investors might have their own particular political views, they’ll have studied the outcome and their wagers represent especially informed opinion.

This observation is consistent with the argument we made last week that politically-motivated prediction market whales increase the expected returns to non-noise traders, leading to more informationally-efficient markets.

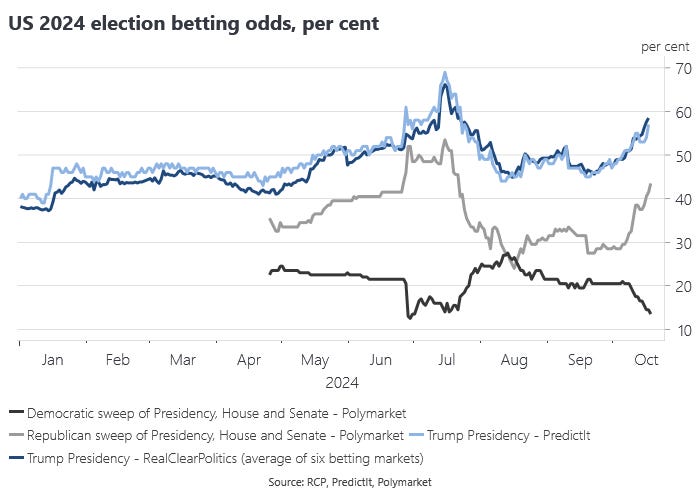

Market participants have been trawling Polymarket’s central limit order book in search of whales and would appear to have found one. Long story short, the whale is not who you might expect, but that just underscores the fact that the whale’s identity is mostly an irrelevance. The implied probability of a Trump victory has surged across a range of markets, including the share price of Trump Media and it would be a mistake to dismiss this as just a function of a single politically-motivated trader placing big bets on Polymarket, a crypto-based exchange with Trump-aligned ownership.

Trump’s improved betting market prospects have seen one month rolling correlations with the most obvious of the Trump trades surge to previous highs. To pick just two, the correlations with both the US term spread and 5y5y forward inflation expectations have turned strongly positive again. The correlation with the USD is also positive, which is consistent with our thesis that Trump’s policies are perversely USD positive, despite (or perhaps because of) Trump’s preference for a weak dollar policy.

Fresh from cursing global housing by declaring a housing ‘super cycle,’ The Economist magazine has also just given a nice contrarian warning signal for the US economy on election eve. While I have also consistently highlighted the outperformance of the US economy, by the time it makes the cover of The Economist that outperformance must be viewed as largely priced.

Brent Donnelly has been keeping score and his total return on shorting The Economist’s cover stories is running at 214% with a win rate of 67%.

His preferred trade for shorting the US economy is long TLT rather than short USD. I agree on the latter point, but long TLT runs opposite to the canonical Trump trade, which assumes a bear steepening in the US yield curve on increased duration risk. It is one thing to short the US in a cyclical sense, which is the point of Brent’s proposed contrarian trade on The Economist cover story, quite another to short the US in a structural sense. The Trump trade is more about the latter, in which a Trump Presidency is a negative supply shock that is somewhat orthogonal to the business cycle.