Mind the gaps

Output gap measures in the US, Japan, Canada and Australia

Output gaps attempt to decompose real GDP into cyclical and trend components. The cyclical component reflects the demand pressures that predict inflation and are of most interest to monetary policy. Output gap measures are a solution to a latent-variable extraction problem, in which the latent variable is the equilibrium level of output. The non-accelerating inflation rate of unemployment (NAIRU) is the labour-market analogue to this level of output.

There is no unique solution to the problem of recovering an unobservable variable like potential output. Some output gap measures are based on statistical filtering techniques, some are estimated based on capacity utilisation measures, others on a production function approach. All output gap measures are imperfect. The relevant test for monetary policy purposes is whether they have predictive power for inflation. Where that predictive power breaks down, we have reason to believe inflation is being driven by something other than aggregate demand, at least in the absence of structural change.

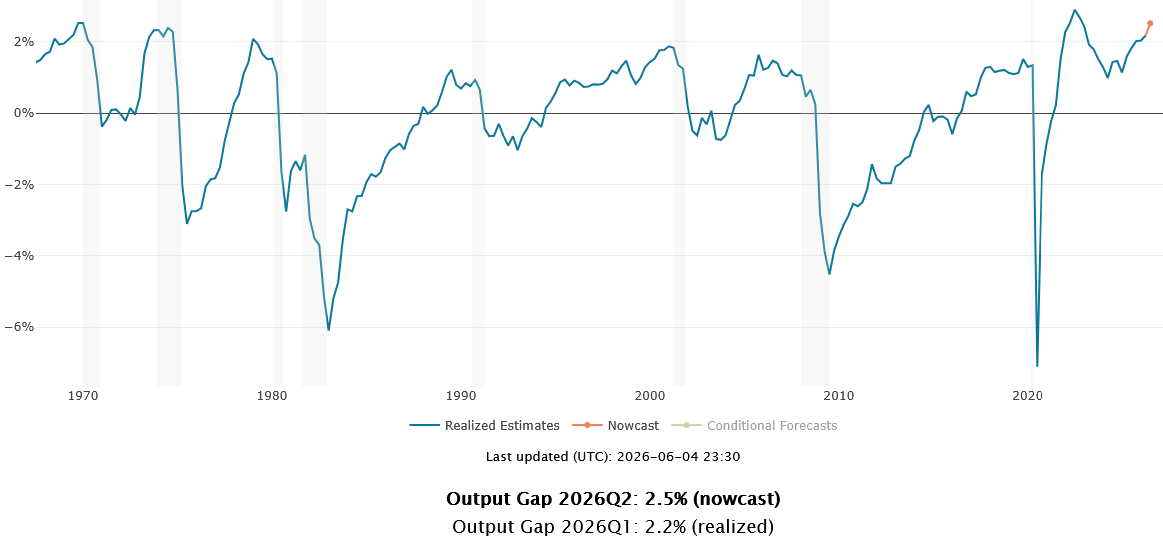

The Berger, Morley and Wong (BMW) approach to nowcasting the US output gap has been yielding an increasingly positive gap in recent quarters. The Q1 output gap is put at +2.2% and nowcast at +2.5% for Q2.

An increasingly positive gap perhaps explains the recent pick-up in inflation, abstracting from the oil price shock. The BMW measure has recently been modified to take account of what the authors suggest is a structural break in the level of consumer sentiment and its relationship to macroeconomic conditions. The University of Michigan consumer sentiment index is at its lowest level since 1952, which hardly seems consistent with a strongly positive output gap of +2.2%. The authors now apply a dynamically de-meaned measure of consumer sentiment in an effort to reflect the break. The US is not the only jurisdiction that has seen a structural shift lower in consumer sentiment post-COVID, one of the more persistent effects of the pandemic.

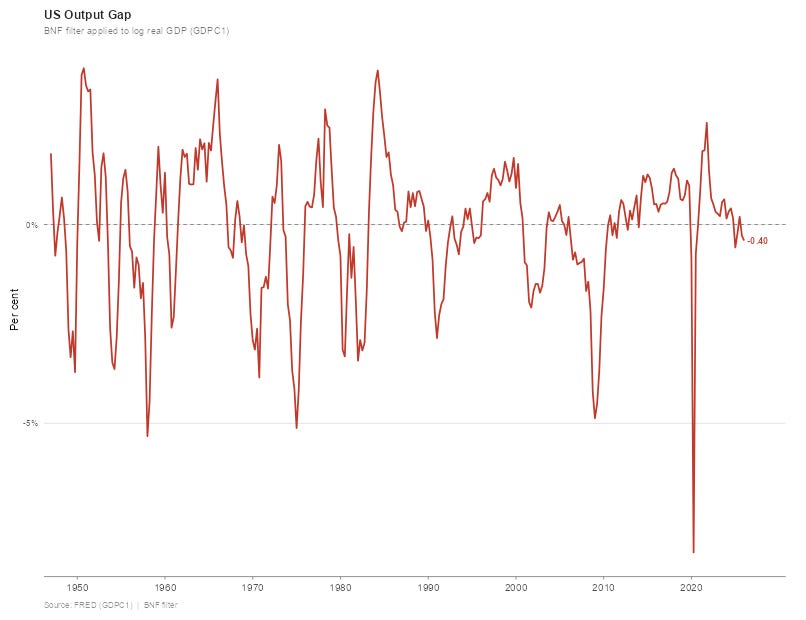

The Kamber, Morely, and Wong (KMW) modified Beveridge-Nelson filter is not reliant on relationships with other variables and points to a US output gap of around -0.4%, which is consistent with the moderation in inflation that saw the Fed easing up until recently, but seems inconsistent with more recent inflation outcomes.

These two measures are worth highlighting, as they show how the same authors can land on very different estimates of the output gap using different approaches. Again, the relevant test for policy purposes is how well they forecast inflation.