Monetary misperceptions and inflation forecast errors: Andrew Hauser’s unintentional case for market monetarism

Plus, the nominal GDP level target that time forgot

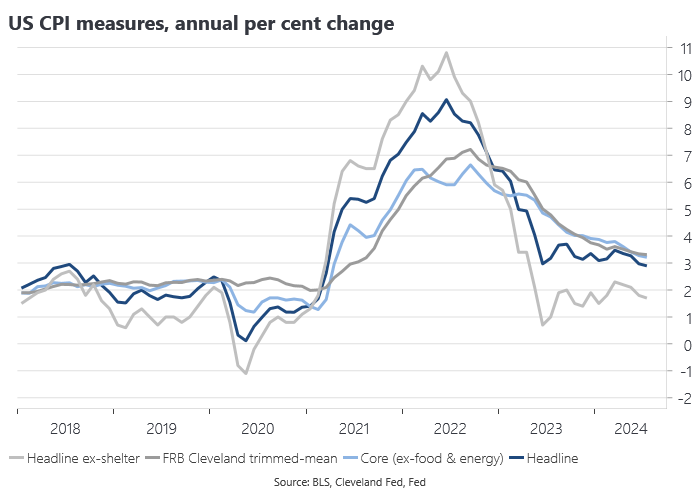

US inflation continued to moderate at an annual rate in July to 2.9% from 3% in June, while the core rate fell to 3.2% from 3.3%, the lowest since April 2021. The CPI ex-shelter fell to 1.7% from 1.8%. On an EU-style HICP basis, which excludes owner-occupied housing, the CPI was also 1.7%. Kevin Erdmann makes a very good case for excluding rents from the CPI for the purposes of monetary policy analysis, noting that rents largely account for the difference between the CPI and the Fed’s target PCE measure. On an ex-shelter/HICP basis, US inflation is comfortably consistent with the inflation target, underpinning expectations for a 50 basis point Fed rate cut in September.

The Cleveland Fed’s trimmed mean measure was unchanged at an annual rate of 3.3%, suggesting the central tendency of inflation is proving more persistent. The US trimmed mean would imply another 0.8% q/q print for the Australian trimmed mean in Q3 based on our simple model relating the two measures.

RBA Deputy Governor Andrew Hauser gave a well-received speech this week on the role of uncertainty in monetary policy decision-making, illustrated in part with reference to the RBA’s inflation forecast errors. As Hauser notes, central bank and market forecast errors have been very similar. Looking at market forecasts for both inflation and the 10-year bond yield in the US based on the following ‘hedgehog’ style charts, it is remarkable the extent to which the forecast errors for both are serially correlated over extended periods, systematically over-stating inflation and bond yields pre-pandemic and then underpredicting them during the post-pandemic inflation shock.

Serial correlation in the forecast error over such extended periods suggests a forecasting process that is systematically biased rather than one that is subject to uncertainty, for which we would expect to see more uncorrelated errors. An obvious source of these serially correlated errors is misperceptions around the stance of monetary policy, in particular, assuming that the pre-pandemic stance of monetary policy was easy because official interest rates were low and that post-pandemic monetary policy was tight, just because interest rates had been raised aggressively. Long-time readers will appreciate that this has been a central element of the market monetarist critique of the conduct of monetary policy in the US and elsewhere over the last decade or so. Without an accurate conception of the effective stance of stance of monetary policy, the resulting monetary misperceptions are bound to give rise to a biased forecasting process and systematic forecasting and policy errors. This is largely because the preferred measure of the stance of monetary policy, the level of official interest rates, is often giving the opposite signal to the one assumed by policymakers.