Nick Whitaker and J. Zachary Mazlish had a good essay at WIP on ‘Why prediction markets aren’t popular.’ Predictions markets are securities exchanges that list binary options on non-financial events, although some of the most popular prediction market contracts relate to financial events for which futures, options and other derivative contracts are also available.

Predictions markets have had a hard time with regulators, but Whitaker and Mazlish:

are arguing against the view that were it not for pesky regulators, prediction markets for everything would be ubiquitous, and that those prediction markets would be the premier way to predict the future. On the contrary, the current size of the prediction market universe reflects market demand. Even if all regulatory hurdles were abolished, we do not expect that universe to dramatically expand.

Theirs is partly a straightforward presumptive inefficiency argument. Given that the regulatory barriers to prediction markets are not as large as many assume, the absence of prediction markets implies that they must be inefficient. Whitaker and Mazlish go beyond the presumptive case to argue that prediction markets lack many of the necessary conditions for the development of deep and liquid financial markets conducive to efficient price discovery.

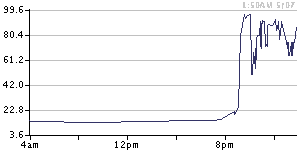

Whitaker and Mazlish decompose market demand into savers, gamblers and ‘sharps’ (informed traders). I prefer a simpler two-sided decomposition into hedgers and speculators. While there are potentially plenty of speculators in any given market, the hedging side is often lacking. There is a well developed futures market for gold because gold producers can use it to hedge against adverse price movements for their output. The demand for hedging North Korean missile launches (an actual contract on the former prediction market Intrade) is less obvious. If your real concern is the implications for the Nikkei, then Nikkei futures are better suited to hedging that exposure.

A 2006 Intrade binary option price chart for a North Korean Taepodong 2 launch.

Macro futures markets

The problem with prediction markets is actually a broader one, extending to macro futures markets. Macro futures markets have also never really taken off, even with wholesale and institutional investors, despite attempts to develop them. Inflation futures are an obvious case where you might expect a deep pool of speculative and hedging demand. Inflation-indexed bonds allow bond market participants to speculate and hedge against inflation, but linkers are well known for being illiquid relative to other government debt securities. As it happens, inflation-indexed bonds proved to be a poor hedge against the recent surge in global inflation because real interest rates also rose alongside the inflation component of nominal rates. These problems have even seen Canada discontinue the issuance of real return bonds.

House price futures also remain under-developed even though there is potentially a very large market for hedging against changes in house prices. I suspect this is largely because housing is a buy and hold market, with typical housing tenures measured in years, if not decades, such that there is little effective demand to hedge short-run cyclical fluctuations in house prices.

In October 2002, Goldman Sachs and Deutsche Bank launched derivatives on economic releases such as non-farm payrolls. Gurkaynak and Wolfers found that these binary options yielded efficient forecasts that were very accurate and at least as accurate as other forecasts. But these contracts were discontinued from 2007 for commercial reasons. This example argues against the notion that these markets are inefficient with respect to price discovery, although supports Whitaker and Mazlish’s point about a lack of demand. Binary options on economic releases were also available on former prediction markets Intrade, iPredict in New Zealand and more recently on Nadex.

A nominal GDP futures market

Along with Scott Sumner, I have been an advocate of nominal income futures targeting, which requires a well-functioning NGDP futures market, ideally made up of wholesale financial market participants, although it would also be good to have ‘mini’ contracts that would facilitate retail participation as well. A nominal GDP futures market could operate on existing futures exchanges and does not require a dedicated prediction market, but arguably suffers many of the same issues that Whitaker and Mazlish have identified in the case of prediction markets. The fact that macro futures markets have little track record to success, despite existing financial market infrastructure to support them, suggests there is an underlying demand problem.

As Whitaker and Mazlish note, where there is a potential positive externality from a prediction or macro futures market, there is also a case for subsidisation to internalise that externality. If the information from a nominal income futures market were valuable to monetary policy decision-makers, then there is a case for a public subsidy, potentially a very large one. The need for such a subsidy only serves to underscore the authors’ point that these markets may not otherwise be viable. As Scott Sumner has argued, a fully credible nominal income futures targeting regime might be characterised by little or no actual trading activity apart from the central bank’s market-making. A more active market would be a sign that monetary policy was losing credibility. A nominal income futures market could be useful to large corporates in hedging their top line revenues, which in many cases would have a relationship with nominal income growth, but it is not clear that nominal income futures would otherwise be a particularly useful hedging instrument.

The chilling effect of regulation

Whitaker and Mazlish briefly mention the potential chilling effect that the threat of regulation might pose to the development of prediction markets. I suspect that this chilling effect is much larger than they allow. Prediction markets may not be completely illegal, but it is enough that they could suffer from adverse regulatory action or proscription after the fact in order to deter their creation. PredictIt is an example of a prediction market that has had its regulatory authorisation withdrawn.

The authors don’t mention the fate of Intrade, a once thriving prediction market, which was hounded out of existence by US regulators. That business had other issues as well, but losing all of its US clients after they were effectively banned from the exchange by US regulators was arguably the death knell. The fact that a prediction market is legal in Ireland, where Intrade was based, is not much help if US regulators can arbitrarily shut down your largest potential client base.

In Australia, OTC binary options, the main contractural form for prediction markets, are currently the subject of a 10 year ban for retail investors by the securities regulator. The ban was put in place as a retail consumer protection measure on the basis that most market participants lose money on OTC binary options, which is a somewhat tautological argument given that these contracts are zero-sum by construction.

I put the ASIC product ban to the test by trying to open an account with a US-based, fully regulated and cash-collateralised securities exchange that provides binary options, but as a ‘sophisticated’ rather than a retail investor. The exchange’s compliance and on-boarding team raised a more fundamental issue than my certification as a sophisticated rather than a retail investor. Since the product intervention order came into effect, they have purged Australia from their sign-up and payments systems. Australia simply does not exist for them. This is entirely understandable, as it is the most straightforward way to ensure compliance with ASIC’s product intervention order. It is also understandable that they are not interested in devoting resources to sifting through the eligibility of different types of Australian client. It is a very good example of the regulatory over-reach I warned about in a previous role when opposing giving ASIC product intervention powers. If the likes of Intrade had not already been killed-off by offshore regulators, they would now be effectively off-limits to Australian clients, ‘sophisticated’ or not, denying these exchanges access to a potentially significant market. These sorts of regulatory interventions are a very real barrier to new entry and prediction markets obtaining efficient scale.

In New Zealand, the prediction market iPredict was killed off by the burden of AML/CTF compliance. This could be taken to prove Whitaker and Mazlish’s point about lack of scale, in that a larger market could perhaps afford to incur these regulatory costs, but these regulatory burdens remain a significant barrier to entry for any new prediction market, even before they can scale. It is noteworthy that even a small market like New Zealand (population 5 million) was able to sustain a thriving prediction market before being required to comply with the AML/CTF regime. In making the case for a nominal income futures market in Australia, I argued that the regulator should waive regulatory cost recovery on public interest grounds (in Australia, regulated entities are levied by the government to pay for the cost of regulation, but there is provision for a public interest exemption in the cost recovery framework).

The US CFTC has recently ruled that political prediction markets are ‘gaming’ and therefore denied authorisation, but this argument could be extended to almost any event-based contract and so the ruling could be expected to have a significant chilling effect on the further development of prediction markets. Kalshi’s battle to establish a political events market in the US has only served to underscore the generally hostile position of regulators (see the amicus briefs in Kalshi’s litigation against the CFTC).

Commissioner Summer K. Mersinger's dissent on the CFTC's ruling said that:

The fact that certain portions of the Proposal are inaccurate, extremely weak, or simply make no sense suggests that it either was hastily prepared, or is motivated primarily by the sheer hatred that the Commission seems to bear towards event contracts.

In the mid-2000s, I was able to trade event contracts on Intrade in Ireland, Nadex (formerly Hedge Street) in the US and iPredict in NZ. Intrade and iPredict were killed off by US and NZ regulators, while Nadex is effectively proscribed by Australian regulators. I would argue that the regulatory barriers to prediction markets are significant, making it difficult to draw firm conclusions about whether prediction markets can successfully scale. Indeed, the cost of regulation makes it difficult to launch even conventional wholesale futures and other markets in Australia.

We are fortunate that there are entrepreneurs still willing to push the envelope on prediction markets in the US, despite the regulatory hostility. The inefficiency case against prediction markets would be much more convincing if the regulatory environment were more supportive.

ICYMI