So much winning, you’re not going to believe it

Plus, is China ‘the world’s most productive economy’?

The big winners from the US Presidential election, apart from Trump himself, were Polymarket’s French whale (with a P&L ~$48 million), along with Hanson and Oprea, whose model helps explain why a trader with additional quadratic preferences can improve the accuracy of prediction markets. As it turns out, Théo the whale was an informed rather than a noise trader who relied on neighbour polls to conclude that Trump would win and even commissioned his own neighbour polling to verify their accuracy. This was a textbook case of prediction markets surfacing tacit or distributed knowledge (not that many textbooks teach the value of prediction markets).

Despite a late slump on the Iowa Ann Selzer poll, prediction markets mostly gave a high probability to a Trump victory in the run-up to the election relative to that suggested by the poll-based election models. It is also worth noting that prediction markets had been showing a steady improvement in Trump’s prospects since the beginning of 2023. A Republican sweep was almost invariably given a much higher probability than Democrat sweep.

For all the regulatory impediments to the functioning of prediction markets, their pricing looks remarkably efficient (a separate issue from being correct ex post). Reportedly, the French government now wants to ban Polymarket in its jurisdiction, apparently wanting to shoot the messenger after it has spoken. If the whale isn’t launching a ‘high conviction’ long-only equity fund off the back of his winnings, he is missing a great marketing opportunity.

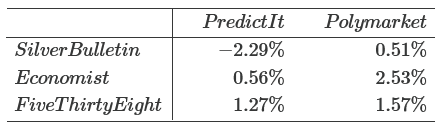

Of the election models, Nate (‘I ran 80,000 simulations’) Silver’s did the worst when benchmarked against a prediction market P&L. His model would have lost money regardless of who won the election. PredictIt was the hardest market for the models to beat, based on Rajiv Sethi’s trading simulation:

In a now notorious tweet, Silver confused cross-section variation in income with inflation to estimate a swing against the incumbent. His substantive point was surely correct (it’s been a feature of macro models of the vote share like Ray Fair’s for decades), but the way he got there was nonsense. Paul Mainwood notes that the poll-based election models in 2024 did a better job of forecasting the 2020 than the 2024 election. This suggests an over-fitting problem, in which the pollsters are always fighting the last war. For its part, The Economist gave Harris an edge of 56% in its election eve update (who said it pays to be Bayes?).

It should surprise no one that Scott Sumner called the election back in November 2023. As Scott said back then:

I don’t believe the pundits are wrong about Trump, I believe they are wrong about America.

Never short Scott Sumner.

Tired of winning

Trump at least won by fair means and not foul. An attempted Trump putsch would have been a risk given a much narrower result. Trump is still a danger to US institutions, but now has the option to bend them to his will over time rather than try and smash them upfront. The bending could be an even more insidious process and US and global institutions might still eventually break rather than bend.

We have spent much of this year hashing over Trump’s substantive policy proposals and their implications and won’t revisit those earlier posts here. Broadly speaking, the prospective trade war, policy uncertainty and mass deportation of unauthorised workers can be expected to offset any benefits that might flow from tax cuts and deregulation. The highest tariff rates since the 1930s will leave every business in the US beholden to the executive for exemptions and effectively at Trump’s mercy. That will be an enormously corrupting influence on US politics and society.

The pre-election Trump trade continues to have legs given that a Republican sweep was not fully priced but at some point markets will have to reconcile higher interest rates and higher equity prices. The risk-on trade will eventually give way to increased risk aversion as Trump unleashes chaos on the US and global economy. The interventions will beget more interventions. Risk premia will rise and volatility will increase. Low vol and defensive equities will at least capture the risk premia with less volatility. The US can still be expected to outperform on a relative basis if only because of negative international spillovers from Trump’s policies. Trump is not just a problem for the US. He’s everyone’s problem now.

January 6 2021 should have been the end of Trump. We said before that the failure to deal with him decisively then was a first-order institutional failure from which the US may never recover. The standard you walk past is the standard you accept and that standard is now President-elect.