The dollar bloc inflation shock: FAIT versus FIT

A late-cycle comparison

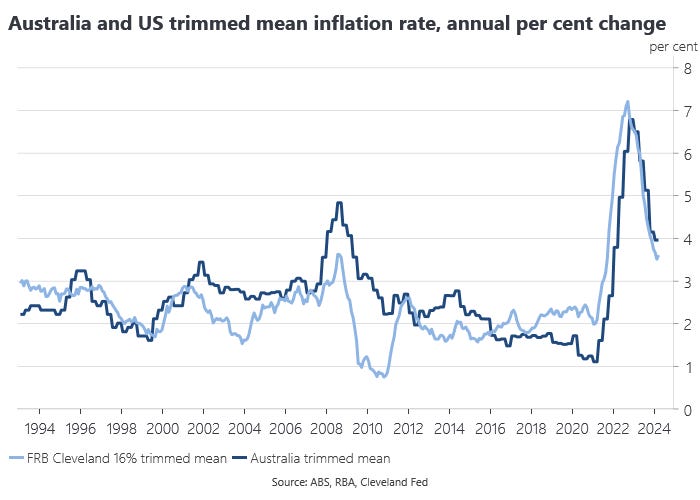

Australia’s first quarter inflation rate came in higher than expected, once again highlighting its relatively drawn-out disinflation process and pointing to the prospect of yet another late-cycle tightening.

The headline CPI rose 1.0 per cent over the March quarter and 3.6 per cent over the year, compared to 4.1 per cent for the year-ended in the December quarter. This was stronger than the 0.8 per cent quarterly and 3.5 per cent annual increase financial markets were expecting for the headline measure.

The trimmed mean inflation rate rose 1.0 per cent over the quarter and 4.0 per cent over the year. This was also stronger than the 0.9 per cent quarterly increase financial markets had expected on this measure, which was also what we were expecting based on our model..

Australia is still lagging the US disinflation process, benchmarked here against the Cleveland Fed’s trimmed mean inflation rate.

Trimmed mean inflation is running 0.4 percentage points higher than the RBA was forecasting for the middle of this year in its February Statement on Monetary Policy. Trimmed mean inflation only just squeaks into the target range at the end of 2024 based on those forecasts and doesn’t approach the middle of the range until 2026. A significant upward revision to the inflation forecast in the May Statement on Monetary Policy is not likely to be consistent with the inflation target, but could always be nudged back down with another increase in the cash rate.

A late-cycle comparison

This is an opportune time to review the post-pandemic experience with inflation across the dollar bloc economies: the US, Australia, Canada and New Zealand. Monetary policy in the rest of the dollar bloc is not completely independent of the Fed given international spillovers from US policy that serve to tighten global monetary conditions. The non-US dollar bloc economies are price takers in global capital markets and we would expect their economies and interest rates cycles to be broadly correlated, if not synchronised. The four economies have very similar nominal anchors, with inflation targets of 2 per cent, although the RBA targets a somewhat higher 2.5 per cent as a central tendency for its inflation rate. I ignore the relative experience with fiscal policy on the basis it is effectively discounted in the conduct of monetary policy.

The four economies all experienced a post-pandemic inflation shock attributable to both supply and demand-side factors. The supply shock associated with Russia’s renewed invasion of Ukraine in February 2022 was something central banks appropriately looked through, but this diverted attention from the underlying demand shock that was also driving inflation pressures.

In the US, the failure to contain inflation is widely attributed to the Fed’s operationalisation of its new flexible average inflation targeting framework (FAIT) from August 2020. In particular, the FOMC’s asymmetric interpretation of FAIT is said to have given US monetary policy an inflationary bias. However, the post-pandemic experience with inflation is broadly similar across the other dollar bloc economies. These economies maintained their pre-pandemic flexible inflation targeting (FIT) frameworks, notwithstanding some very recent changes, arguing against the idea that the adoption of FAIT and its implementation by the FOMC was the main factor determining US inflation and other macroeconomic outcomes.

Other dollar bloc economies suffered similar inflation shocks, despite more timely changes in the notional, if not the effective, stance of monetary policy. US macroeconomic outcomes at the end of 2023 look favourable compared to the rest of the dollar bloc. New Zealand implemented the most timely response to the inflation shock, but has suffered some of the worst macroeconomic outcomes. Australia is something of any outlier in this comparison, having mostly lagged its dollar bloc peers, with a drawn out disinflation process and late cycle tightening.

Price level comparison

Comparing the evolution of the price level since the beginning of 2021 shows the United States experiencing a higher increase in its price level compared to the other three economies measured on a CPI basis. However, on a PCE basis, the Fed’s target measure, the US experience of inflation has been in line with the FIT economies. Indeed, with the exception of New Zealand, the increase in the overall US price level on a PCE basis is very similar to the increase in the CPI in the FIT economies by March 2023 and has been broadly similar since. Inflation in Australia is less pronounced in the early stages of the inflation shock in 2022, but then converges with the US and Canada, while New Zealand’s price level increase has been more pronounced.

Inflation rate comparison

The four economies all experienced an acceleration in inflation in the first half of 2021. Comparing inflation rates, the US has a more pronounced inflation shock on a CPI basis, at least until October 2022, when the US CPI inflation rate starts to fall below Australia and New Zealand and closely follows Canada. On a PCE basis, the US begins to disinflate from the middle of 2022 and has been consistently below the FIT economies from August 2023. The US experience of disinflation has been similar to that of Canada, while Australia and New Zealand have seen more moderately paced disinflations.

Comparison of policy rates

Official interest rates are a poor measure of the effective stance of monetary policy, but are at least indicative of the intended or notional stance of monetary policy. The timing of a change a policy rate is also indicative of a change in the central bank’s evaluation of the economic outlook. The four central banks all go into the inflation shock with their policy rates ‘bounded’ at between zero percent and 0.25%. Given a similar starting point, the subsequent change in the nominal cash rate serves as a comparable benchmark for the notional stance of policy. Once policy rates were lifted from their respective ‘floors,’ quantitative approaches to policy were largely sidelined as monetary policy operating instruments and in official accounts of the stance of policy.

The RBNZ is the first of the four central banks to raise its policy rate in October 2021, followed by the Fed and the BoC in March 2022 and the RBA in May 2022. At the time the RBNZ tightened in October 2021, it had a higher CPI inflation rate than its dollar bloc peers with the exception of the US and the RBNZ has presided over more a more aggressive tightening cycle economies comparable to that of the Fed. The RBA lags the other three central banks, particularly from September 2022 and continued to tighten into the end of 2023, with further tightening partially priced for 2024 following the March quarter CPI release.

Adjusting policy rates for inflation allows a comparison of the extent to which changes in interest rates have offset increases in inflation to change the real interest rate, consistent with the Taylor principle that the policy rate should move more than one for one with the inflation rate. The Fed is the first central bank to see a meaningful lift in its real policy rate from March 2022, closely followed by the RBNZ in May and the BoC in June 2022. The RBA follows in August 2022. Both the RBA and RBNZ notably lag the Fed and BoC on this measure from the second half of 2022.

Comparison of nominal GDP

Changes in nominal GDP are a sufficient description of the effective stance of monetary policy and the four economies show a variable evolution of nominal GDP in the post-pandemic period. The US and Canada converge in Q1 2023. Australian nominal GDP growth outperforms New Zealand. New Zealand experiences a double-dip recession in real output in Q4 2022 and Q1 2023 and in H2 2023, offsetting relatively high inflation pressures. Australia ends 2023 with a level of nominal income around 6 per cent higher than New Zealand relative to their respective pre-pandemic levels.

Comparison of nominal exchange rates

Following Sumner’s price of money approach, we can view the evolution of the nominal effective exchange rate as a proxy for the stance of monetary policy, at least over short horizons. Relative to the start of 2021, only the US shows an appreciation in its exchange rate. The US dollar has a large weight in the effective exchange rates of the other economies, so it is not surprising that they show a depreciation over the same period. The Canadian dollar appreciates in early to mid-2021, consistent with its early exit from quantitative easing and depreciates less relative to the US dollar than AUD or NZD. NZD shows the largest depreciation, suggesting monetary conditions remain relatively easy despite a relatively aggressive tightening cycle in terms of the nominal cash rate and a weaker nominal GDP performance.

Comparison of real output

By the end of 2021, all four economies recovered their pre-pandemic levels of output, with Canada lagging somewhat. Australia and New Zealand outperform, although New Zealand peaks in Q3 2022 before suffering a double-dip recession, with the level of output at the end of 2023 below its post-pandemic recovery peak. The US ends 2023 with the highest level of output relative to pre-pandemic levels.

Comparison of employment levels

All four central banks have mandates that variously require them to take account of the sustainable level of employment, although the RBNZ reverted to a single price stability mandate with the change in government in October 2023. Australia and New Zealand have relatively modest pandemic downturns in employment due to pandemic labour market interventions that focused on job retention rather than the US approach of increased transfer payments.

By the end of 2021, Australia, Canada and New Zealand recovered their pre-pandemic levels of employment, whereas the US does not recover until mid-2022. Australia’s employment growth outperforms from early 2022 as its disinflation process starts to lag. The relatively slow US labour market recovery may account for the less timely policy response to the inflation shock in 2022 relative to Canada and New Zealand. It has been suggested that the August 2020 FAIT framework led the Fed to overweight employment in its post-pandemic reaction function, delaying Fed tightening, but the timing of its post-pandemic tightening cycle is similar to that of the other central banks with better labour market outcomes, so the labour market does appear to be the decisive factor in timing lift-off in policy rates.

Summary

Relative to the FIT dollar bloc central banks, the Federal Reserve under FAIT does not appear to significantly underperform its peers in its management of the post-pandemic inflation shock. The asymmetric interpretation and operationalisaton of FAIT, which has focused on the ‘flexible’ part of the framework, has left Fed policy close to that of the FIT central banks in both theory and practice, with broadly similar macroeconomic outcomes.

The initial change in the notional stance of Fed policy is less timely than the RBNZ and BoC, but more timely than the RBA. The US ends 2023 with a post-pandemic price level equal to or lower than that of other economies on its target measure, although with higher inflation on a CPI basis. The US experiences an increase in the level of real output similar to that of the other economies and outperforms more recently.

The US disinflation process has led that seen in the other economies and the US now enjoys a lower inflation rate on its target measure, despite a more significant shock to the level of the CPI. The RBNZ implemented a more timely and aggressive initial monetary policy response, with an overall increase in its policy rate of similar magnitude to the Fed, but has seen worse macroeconomic outcomes on most measures, including a double dip recession in 2022 and 2023. This in turn has prompted a change in the RBNZ’s monetary policy remit to a more singular focus on inflation following a change in government in October 2023. The RBA has mostly lagged its dollar bloc peers into terms of the timeliness of its monetary policy response and with a more drawn out disinflation and tightening cycle, but with relatively favourable employment and real growth outcomes.

As the Fed approaches its 2025 monetary policy strategy review, it is worth reflecting on the comparative experience of other central banks. It is not obvious that US monetary policy under FAIT has underperformed the FIT central banks, but that may reflect the fact that FAIT has been closer to FIT in its implementation than its original conception.