The neutral real interest rate doom-loop

The neutral real interest rate doom-loop

Plus, why nominal income targeting is compatible with the existing inflation target

The minutes of its July meeting showed that the RBA Board had a discussion on the neutral real interest rate. Governor Lowe elaborated on the theme in his speech to the Australian Strategic Business Forum last week. The bottom line is that the RBA views the neutral real interest rate as at least positive, with the implication that the neutral nominal rate is at least 2.5%, assuming inflation expectations evolve in a way consistent with the inflation target. Lowe noted that the neutral rate serves mainly as a benchmark for whether interest rate settings are expansionary or contractionary and that ‘we are not on a pre-set path to achieve any specific level of the cash rate.’

The discussion in the Board minutes brought to mind the notorious (to me at least) discussion of the same concept in the July 2017 Board minutes, which contended:

Yet over the proceeding five years, nominal GDP averaged an annualised growth rate of 3.6%, while the average trimmed mean inflation rate only scrapped into the bottom of the target range at 2.1%. At the time of the July 2017 Board meeting, the trimmed mean inflation rate was running at annual rate of 1.7%. The claim that monetary policy was expansionary was far from obvious from the data. If anything, the effective stance of policy looked modestly restrictive.

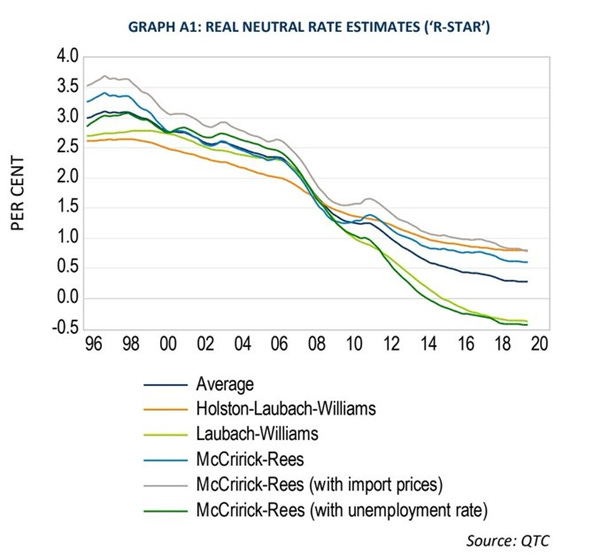

This episode supports our long-standing contention that evaluating the stance of monetary policy based on the level of the nominal interest rate is likely to be misleading. Conditioning policy on an unobserved variable (as opposed to an observable like nominal GDP) is likely to lead to policy errors. Trent Saunders from QTC illustrates the range of pre-pandemic estimates for Australia from just a few of the main approaches used in estimating the neutral real rate:

Forecasting the terminal cash rate this cycle based on an estimate of the neutral real interest rate strikes me as a very fraught exercise. As Scott Sumner has often argued, the equilibrium real rate is not independent of the stance of monetary policy. In particular, overly tight monetary policy is likely to lower the equilibrium real rate. This can set in train a doom-loop in which insufficiently accommodative monetary policy chases the equilibrium real rate lower. This would seem to describe US monetary policy post-GFC and Australian monetary policy pre-pandemic.

RBA review

The review of the RBA has a web site, so watch that space for future developments (you can also sign-up for email alerts). The announcement of the review occasioned some pushback from those who argue that it would be a mistake to change the existing inflation target. But this opposition misses at least two points. First, the RBA itself effectively walked away from the inflation target from 2016 onwards when it chose to prioritise financial stability. An important question for the review to address is not just the merits of inflation targeting, but why the RBA sought and obtained from government a license to move away from it via the extant Statement on the Conduct of Monetary Policy. One finding of the review could well be that the RBA lost its way when it comes to best practice in inflation targeting and needs to get back on track. Even taking the existing 2-3% target range as given (I have no issue with the range as such), there are still numerous issues around the specification of the target, much less its operationalisation, that the review could address.

Second, like other advocates of nominal income targeting, my suggested nominal GDP growth path assumes an equilibrium inflation rate of 2.5%. While nominal GDP targeting allows for deviations in inflation from that equilibrium rate, the overall target specification still anchors the inflation rate (a point often made by Warwick McKibbin).

Nominal income targeting is not a repudiation of inflation targeting, but a re-specification of the RBA’s reaction function that can embed the same target. One of the points I tried to make in estimating an implied nominal GDP targeting rule for Australia is that such a target is not a radical departure from the historical reaction function. Indeed, my estimated rule had the best fit with the actual cash rate during the Golden Age of inflation targeting under Governor Macfarlane. That’s not a coincidence. The point of nominal income targeting is to help the RBA do inflation targeting better, by minimising the risk of perverse monetary policy responses to temporary supply shocks, a useful property in the current environment. The knee-jerk defence of the current inflation target overlooks these considerations.

Q2 inflation

Wednesday’s Australian Q2 CPI release has the market expecting 1.5% q/q and 4.7% y/y for the key trimmed mean measure, which captures the persistent component of inflation of most concern to the RBA. As noted in a previous post, our preferred model is calling it at 1.6% q/q and 4.8% y/y, which will maintain expectations for a further 50 bp of tightening at next week’s RBA Board meeting.

ICYMI

My obituary for Tony Makin in The Economic Record. Thanks to the editor, Renee Fry-McKibbin, for inviting me to contribute this piece in Tony’s memory. Thanks also to those who shared their recollections of Tony’s life and work with me.

I have a new report out with the Fraser Institute, co-authored with Milagros Palacios, The Canadian-Australian Business Sector Productivity Gap: A Sectoral Analysis.

Peter Tulip discusses the review of the RBA (video).

Trump’s plan to seize control of the US administrative state in 2025.

The JPY begs to differ! ‘Bank of Japan Should Stop Meddling in Financial Markets: There is no evidence that buying stocks and bonds has had the desired effect of stimulating activity and inflation in the country.’ It is contradictory to argue that monetary policy distorts financial markets, but is also ineffective.

How are those JGB shorts working out for you?

Scott Grannis on the BTC-SPX correlation. As argued here previously, the fact that BTC is no longer a counter-cyclical asset is a positive from the point of view of mainstreaming crypto.

No evidence for nudging after adjusting for publication bias. Further background here:

Your tweets:

Looking for neutral rates (or potential output or natural unemployment) is like "looking for Wally when there are many Wallies!

https://thefaintofheart.wordpress.com/2015/10/25/looking-for-wally-when-there-are-many-wallies/