The New Zealand economy and monetary policy: the RBNZ left its mandate outside the dairy, nek minnit

The New Zealand economy and monetary policy: the RBNZ left its mandate outside the dairy, nek minnit

Plus, US August #NFPguesses: looking for another big gain in payrolls employment

This week, we are going to take a look across the Tasman and see what our kiwi cousins have been up to. As a small open economy and commodity exporter, New Zealand is on the front line of the global business cycle and is always a useful cross-check on what is happening elsewhere in the dollar bloc. New Zealand has also often been at the forefront of innovations in monetary policy governance, although not always in a good way. Its monetary framework is worth examining for lessons it might hold for other jurisdictions. So let’s start there.

The RBNZ’s monetary policy framework

The RBNZ’s monetary policy framework has gone through many iterations since the RBNZ Act 1989 came into operation in 1990. The shift to a multi-member proportional voting system since the 1996 general election has meant that coalition governments have been the norm in New Zealand and each new government has taken a stab at the monetary policy framework. There has been a steady dilution of the original singular focus on price stability through the introduction of other considerations for policy, as well as a shift away from the single-decision maker/accountability model.

In my then day job in 1997, I was visiting clients at the RBNZ in Wellington. Then Governor Don Brash heard I was in the building and asked me to come up and discuss my then recently published CIS monograph on central banking, which he had read. It was a very wide-ranging discussion, the sort of interaction that is only possible in a small place like New Zealand. A lot has changed since then, but inflation targeting is still central to the RBNZ’s monetary policy framework.

The latest amendments to the RBNZ Act came into operation on 1 April 2019 and added an employment objective to the RBNZ’s long-standing price stability objective and created a formal Monetary Policy Committee (MPC) with members internal and external to the RBNZ.

In 2021, a new remit was issued requiring that in the secondary considerations, the MPC should assess the effect of its monetary policy decisions on the current government’s policy of more sustainable house prices. These changes are currently the subject of a formal review process.

I don’t propose to hash over the merits of these recent changes here. While I have long opposed making house prices a consideration for monetary policy (except insofar as house prices contain useful information about the state of the economy), in practice, I think the RBNZ only pays lip service to this objective. It is at worst an unhelpful distraction on which the RBNZ’s staff now have to waste their time.

The RBNZ has come in for considerable criticism in recent years in relation to issues of governance, culture, research, staffing, as well as monetary policy implementation. New Zealand Treasury is not faring much better. Research output from both institutions has collapsed. An open letter from former RBNZ official Geoff Mortlock summarises many of these concerns. Another former RBNZ official, Michael Reddell, has a blog largely devoted to his criticisms of the institution. My focus below will be recent macroeconomic outcomes rather than institutions, but it worth noting that institutional weaknesses are likely to pose the most serious problems when the Bank’s credibility is being challenged by adverse shocks.

Recent developments in the New Zealand economy

Let’s start with headline growth.

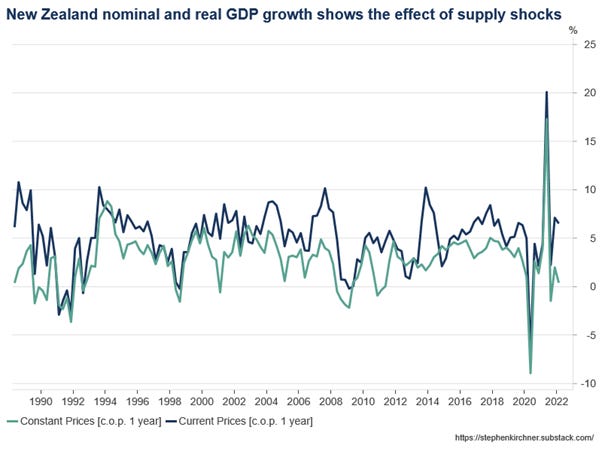

The real economy contracted 0.2% in the first quarter and expanded only 1.2% over the year. By contrast nominal GDP rose 1.9% q/q and 8.6% y/y. The large wedge between nominal and real GDP growth is indicative of an economy being hit by a supply shock, but is also symptomatic of an excess demand problem. Trend annual nominal GDP growth in New Zealand is around 5%. New Zealand’s inflation target mid-point is 0.5 percentage points below Australia’s and trend real growth is a touch lower, so we would expect a slightly lower trend growth path for nominal GDP.

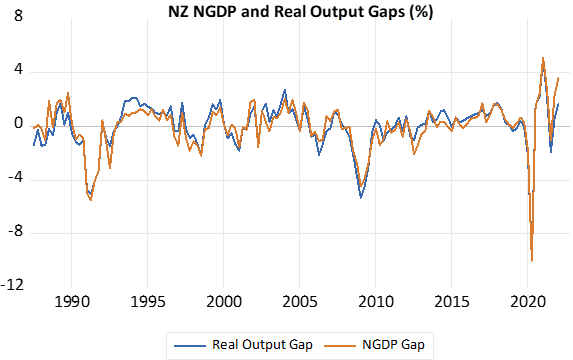

My estimate of the real output gap in NZ is 1.7%, while the NGDP gap is 3.6% (based on a modified Beveridge-Nelson filter):

Above-trend NGDP growth and a positive NGDP gap can be taken as symptomatic of an excess demand problem. However, like Australia, New Zealand’s terms of trade is at record highs, which contributes to nominal GDP growth, but is also symptomatic of the global inflation pressures to which New Zealand is subject.

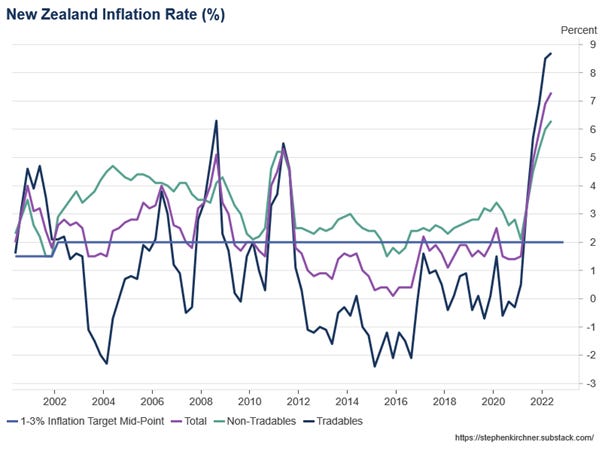

Looking at inflation, both tradeables and non-tradeables inflation is running hot and well above target.

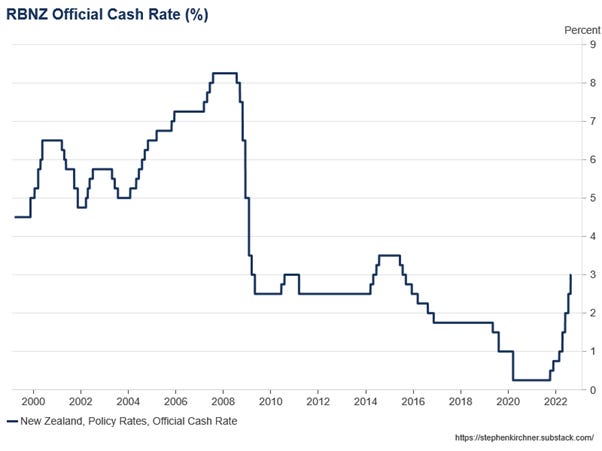

The RBNZ began a new tightening cycle in October 2021 with a 25 basis point rate hike that has since taken the OCR from 0.25% to 3.0%.

On 23 February 2022, the Monetary Policy Committee agreed to commence the gradual reduction of the RBNZ’s bond holdings under the Large Scale Asset Purchase (LSAP) programme through both bond maturities and managed sales starting in July. So quantitative tightening will reinforce the increase in the cash rate.

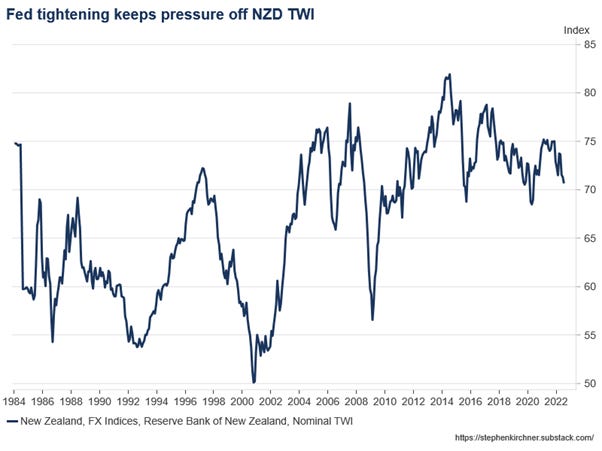

Increases in the NZD exchange rate have historically been one of the most problematic elements of previous RBNZ tightening cycles and a source of discontent for exporters. This tightening cycle, Fed tightening is helping to keep the pressure off the NZD TWI, but this increases the burden on the cash rate in tightening overall monetary conditions.

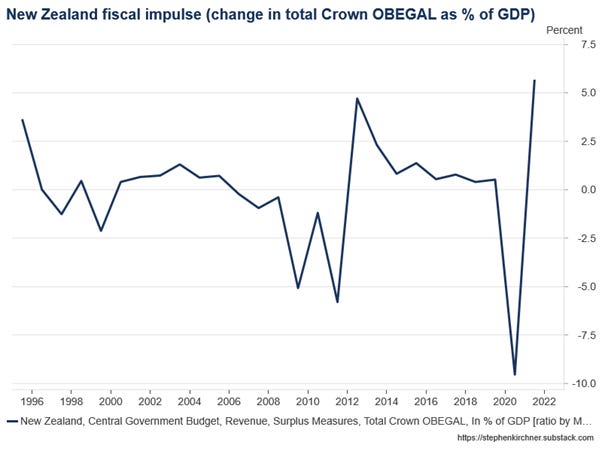

Narrow money supply growth has moderated and the yield curve has been flirting with inversion, which is not uncommon in New Zealand. The fiscal impulse has also turned contractionary.

Like Australia, New Zealand’s unemployment rate is at multi-decade lows, while job vacancies are at record highs, consistent with the theme of tight labour markets globally. However, to be consistent with the ‘sustainable’ part of its ‘maximum sustainable employment’ mandate, more labour market slack is going to be required. Preferably, this would come through increase labour supply rather than through crushing labour demand with tight monetary policy. Labour costs are growing rapidly.

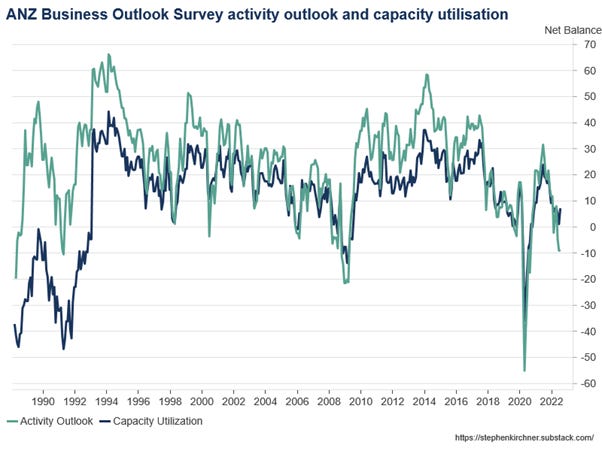

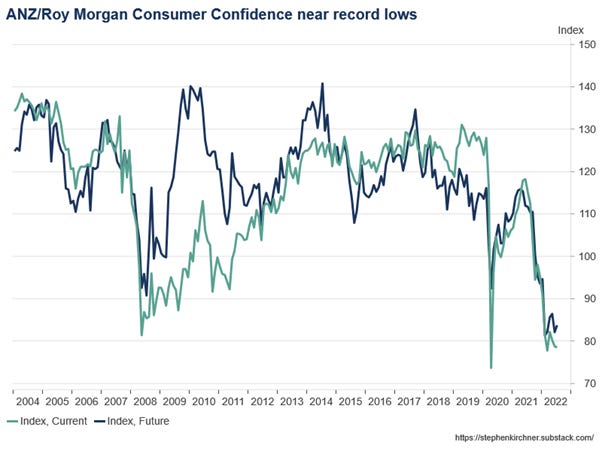

Capacity utilisation has been declining and both business and consumer sentiment are very weak. Again, this is similar to trends we have seen globally, where sentiment data has taken a hit from higher inflation and interest rates, but the vibe-cession also seems to be weighing on activity in NZ.

As a small open economy, New Zealand is particularly vulnerable to domestic supply constraints and global supply shocks. The RBNZ faces a difficult task returning inflation to target. As in other economies, the main risk is that monetary policy continues to respond to supply shock-driven inflation well past the point that aggregate demand is already moderating.

My friends at the New Zealand Initiative recently published a paper highlighting what they say were mistakes made by central banks after 2019. I am more forgiving given the nature of the pandemic shock. The RBNZ’s inflation problem is partly due to its aggressive monetary policy response to the pandemic in a country that locked-down heavily. That is not obviously a mistake, even ex-post, given the nature of the shock. For mine, the more serious policy error, common among central banks, was below-target inflation pre-pandemic.

US August #NFPguesses

Our model is pointing to another big 586k gain in non-farm payrolls employment in August, with most of the model inputs pointing higher this month. The market is expecting 270k after July’s 528k increase, which took the level of payrolls employment 32k above its pre-pandemic level.

I expect the unemployment rate to make a new cycle low at 3.4%, although the market is expecting a steady 3.5%. As we noted last time, on an unrounded basis, the July unemployment rate was strictly speaking a new cycle low not seen since 1969. We only get to 3.4% in August by rounding down and we are conscious of the fact that our models may miss the turn at prospective cyclical highs/lows for payrolls/unemployment rate. Given the likely impact of another big gain in payrolls on Fed sentiment, brace for perverse responses from markets.

ICYMI

Federal funds futures do not have forecasting power for future bond returns and term premiums.

Fasten your seatbelts: How to manage China’s economic coercion.

You like to see it:

Meme stocks: