The Simon-Ehrlich wager over 124 years: The secular trend in real commodity prices

Plus, will Donald Trump run again: the question answers itself

Monday marks the 45th anniversary of the Julian Simon-Paul Ehrlich wager on the trend in real commodity prices. If you are not familiar with the wager, I highly recommend The Bet by Paul Sabin, which recounts the wager and its broader social and political context. The bet is also recounted in John Tierney’s 1990 article for the New York Times Magazine “Betting the Planet.”

The wager was not really about commodity prices as such, but rather the broader political, economic and environmental implications of any trend in those prices. Simon left the choice of commodities and the time frame for the wager to Ehrlich. Ehrlich nominated chromium, copper, nickel, tin and tungsten and a time frame of ten years, commencing on 29 September 1980. If the real price of these commodities rose, Simon was to pay Ehrlich the amount of the price increase and vice versa.

Ten years later, the nominal and real prices of each of the five commodities had fallen, and Ehrlich mailed a cheque to Simon (shown above). Simon then proposed another, larger bet, again leaving the choice of commodities and time frame to Ehrlich. Ehrlich declined the second wager, although proposed a counteroffer along with Stephen Schneider in 1995, which Simon rejected. A recent evaluation (see here and here) of the Ehrlich-Schneider indicators suggests mixed results, whereas Simon’s preferred indicators of human welfare showed significant improvement.

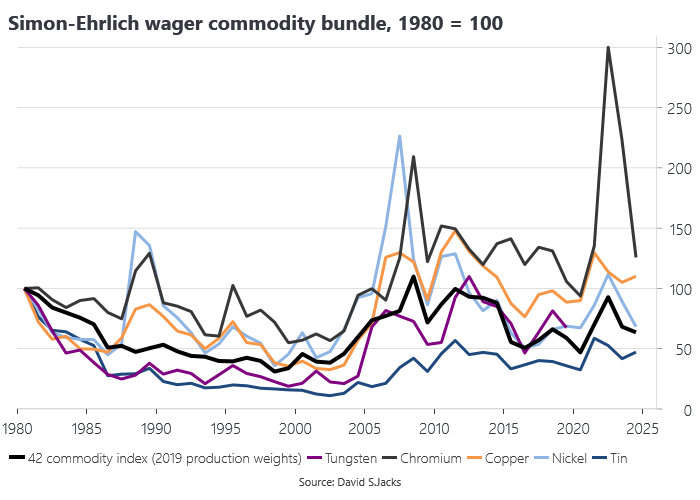

We can check-in how the original Simon-Ehrlich wager is going via David Jacks’ historical commodity price index, which has now been updated for 2024 (I also got the Macrobond people to add the Jacks dataset to their database). Tungsten is not part of his 42-commodity index. However, the USGS provides an inflation-adjusted price series for tungsten from 1900 through to 2019. It is not strictly comparable to the Jacks indices given differences in price deflator, but is good enough for our purposes.

Indexing the Jacks series and tungsten to equal 100 in 1980, we can see how Simon won the original bet, with all five commodities below 100 in 1990. Had the bet been based on all 42 commodities in the Jacks dataset, Simon would have also come out ahead. It was the same story in the following decade, with real commodity prices trending lower through to 2000.

The next decade from 2000 through to 2010 is more complicated. The accelerated industrialisation and urbanisation of China led to a surge in commodity prices that was also responsible for Australia’s terms of trade boom from 2003. The upward trend was interrupted by the 2008 financial crisis, which saw a major downturn in the world economy to close out the decade. These two opposing shocks still left the 42 commodity index lower in 2010 than it was in 1980, although higher than in 1990 and 2000. Of the original Simon-Ehrlich commodity bundle, chromium, copper and nickel were higher in 2010 than in 1980. While the industrialisation and urbanisation of China gave rise to a big cyclical upswing, it is remarkable that global commodity markets readily accommodated this massive transition. Recall that over this period, the majority of the world’s population went from being poor to (in 2018) middle class.

Real commodity prices mostly trended lower in the 2010s. The pandemic shock in 2020 once again saw both the Simon-Ehrlich bundle (not including tungsten) and the broader index lower than they were in 1980. The war in Ukraine has since seen a spike in commodity prices in 2022, with chromium in particular sharply higher given Russia’s significant role in global supply, although even chromium prices moderated in 2023 and 2024. As of 2024, only copper and chromium are higher in inflation-adjusted terms than they were in 1980, with the 42-commodity index lower.

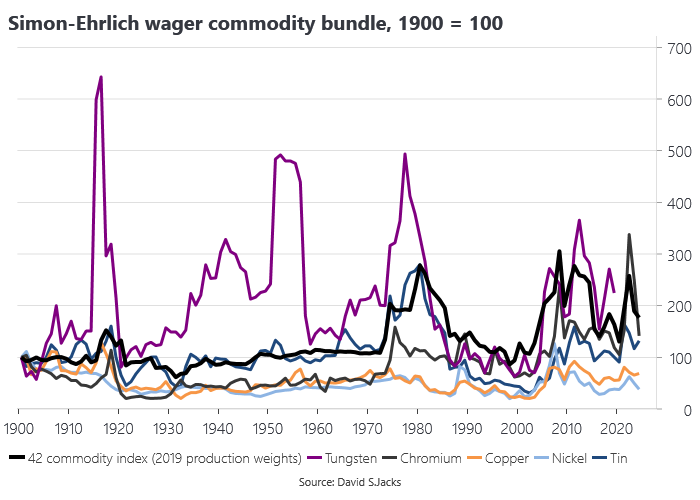

Putting Simon and Ehrlich behind a notional ex post veil of ignorance, we can backdate the wager to 1900 using the Jacks data and ask who would have won a 124-year bet. Only copper and nickel are lower in real terms in 2024 than they were 1900, although this result is largely a function of the China shock in the 2000s and the recent war in Ukraine. Simon unambiguously won the first 99 years of a hypothetical 124-year bet made in 1900.

There have been numerous tests of the Simon-Ehrlich wager showing that the outcome is both window and commodity bundle dependent, as suggested in the above analysis. The Jacks dataset arguably provides the broadest and most definitive long-run measure of real commodity prices, although there are narrower measures with a longer history. His work suggests there is a modest post-1950 upward trend for the 42 commodity bundle, with large medium-run cycles and considerable cross-commodity heterogeneity.

Empirical tests

All bets aside, the trend in real commodity prices is empirically testable, although also a more complicated issue than you might think. Barnett and Morse were among the first to tackle this issue in their 1963 classic, Scarcity and Growth, concluding that resource scarcity did not rise in the US over the period 1870–1957, during which the US transitioned from an agricultural to an industrial economy. Up until the late 1990s, most empirical testing was consistent with a downward trend, but the late 1990s were a major cyclical low in commodity prices. Since the early 2000s, the empirical literature has become more mixed, but if there is an emerging positive trend, as suggested by Jacks, it is very modest and still consistent more consistent with Simon’s optimistic view. Big shocks, like China’s rapid rise, can become influential observations even in very long-run time series. Climate change is another significant shock, although Simon was explicitly optimistic on that challenge as well.

Jacks has also considered long-run trends in commodity price volatility since 1700, finding little evidence of a trend since 1700. Jacks notes:

Three centuries of history shows unambiguously that economic isolation caused by war or autarkic policy has been associated with much greater commodity price volatility, while world market integration associated with peace and pro-global policy has been associated with less commodity price volatility.

Given the direction of travel for US domestic and global geopolitics, we might question whether the long-run trends in the first and second moments of real commodity prices will remain favourable. Simon would certainly acknowledge the potential for domestic and international politics to undo human progress. Real commodity prices are not determined by an exogenously given deterministic trend, but by policy choices within the framework of rules and institutions.

Simon died in 1998 at the age of 65, very close to the peak of globalisation, which would have underpinned his optimism. Ironically, Simon struggled with depression for much of his life and even wrote a self-help book on the subject. Checking in on the 1980 wager every year is a great way to honour his memory and celebrate human progress.

Will Donald Trump run again?

Jeremy Shapiro has a good essay on How and why Donald Trump will run for a third term, which I largely agree with. But the affirmative case is arguably even more straightforward than he suggests. If there were no 22nd amendment, what assumption would you make about Trump’s willingness to run? That’s your answer to the question of whether Trump runs again, because the constitution does not matter to Trump and his enablers. A lot can happen between now and then, but I think the working assumption should be that Trump never leaves office voluntarily. There are many ways by which he might leave office involuntarily, but I think his own preferences are clear enough. That has significant implications for those who have pinned their business, investment and other strategies on just riding out the next four years.

ICYMI

An all star amicus brief in Trump v. Cook.

Why Losing IEEPA Tariff Revenue Won’t Change the Long-Term US Fiscal Trajectory.

A lot of powerful people just don’t realise how unpopular Trump is.

Takatoshi Ito, an early advocate of inflation targeting for Japan, has died at 74. Tak was a regular visitor to Australia and I met him a few times.

Trump is breaking US diplomacy, State Department staffers say.