Too Lowe for zero

The RBA's framework for additional monetary policy tools

The Reserve Bank of Australia has published its Framework for Additional Monetary Policy Tools (AMPT) at low interest rates, alongside an explanatory speech by Assistant Governor (Financial Markets) Christopher Kent. The framework completes a recommendation of the 2023 RBA Review and sets out how the newly constituted Monetary Policy Board (MPB) would approach the design, use and exit from AMPTs in an environment where the cash rate target is at or near zero. It should be read alongside the last two Statements on the Conduct of Monetary Policy, which introduced a section on monetary policy tools, and the changes to the Statement and to the RBA’s governance that followed the creation of two separate boards, a Monetary Policy Board and a Governance Board (GB).

The MPB has, in the words of the latest Statement, ‘the power to do all things necessary or convenient’ to discharge its functions, and the balance sheet and the other boards are subordinate to it for monetary policy purposes. The section on monetary policy tools in the 2023 Statement, and on which the new framework now elaborates, privileges the official cash rate as the main operating instrument for policy and mandates that an exit strategy be specified from the outset for any alternative operating framework.

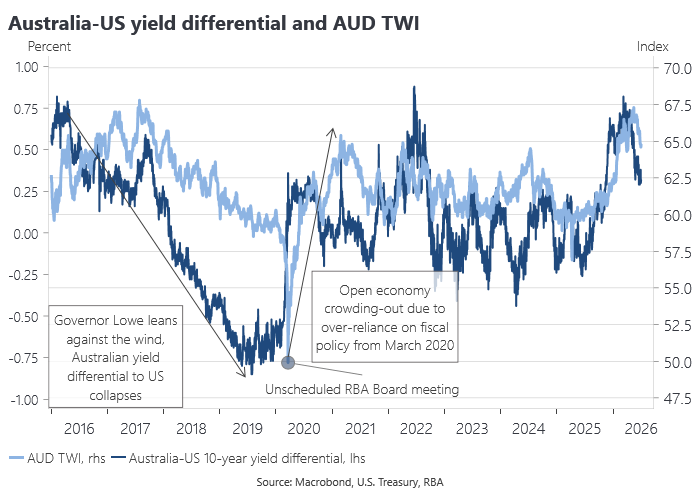

The framework is the product of a particular and, in my view, mistaken reading of pandemic era monetary policy. The RBA’s initial response to the pandemic between March and November 2020 was inadequate. It reflected self-imposed constraints on its main operating instrument, the official cash rate, and delivered a sub-optimal macro policy mix for a small open economy facing a major shock. The Bank’s subsequent reduction in the official cash rate and adoption of a bond purchase program (BPP) from November 2020 effectively conceded the point. The previously claimed effective lower bound was not in fact a binding constraint on policy, the RBA’s balance sheet expansion had lagged that of other central banks; and this put upward pressure on the exchange rate, necessitating the adoption of a BPP.

From November 2020, monetary policy successfully reflated the Australian economy and restored full employment, delivering the lowest unemployment rate in half a century off the back of the worst macroeconomic shock in 100 years. The early exit from the March 2020 yield curve target was a symptom of that success, not a policy failure. The counterfactual – a world in which the RBA held the cash rate steady and defended the yield target into 2024 – would have been a first-order macroeconomic policy failure because it would have implied an extended period of weak economic conditions.

The success and credibility of monetary policy is properly assessed against macroeconomic outcomes, not the notional stance of its operating instruments. Yet the RBA was never able to own its success. The early exit was framed as a policy and credibility failure, and that framing has contributed to the excessive caution now on display in the AMPT framework, in particular, its preoccupation with ‘reputational risk.’ The right lesson to draw from the pandemic episode is the opposite of the one drawn by the RBA Review and which now informs the AMPT framework. The RBA should have adopted AMPTs sooner and far more aggressively than it did.

Oh so conventional

The main conceptual weakness of the framework is its excessive privileging of the official cash rate relative to AMPTs. The cash rate remains ‘our primary and preferred instrument,’ while additional tools ‘are more complex and carry greater risks’ and their effectiveness ‘is also uncertain and depends on the context.’ But many of these observations about AMPTs also apply to BAU under a cash rate targeting framework. AMPTs’ transmission mechanisms and their effects differ in important ways, but we have sufficient local and international experience, especially with BPPs, to be more than comfortable with their use. Even before the pandemic, the RBA’s policy of leaning against the wind brought the cash rate close to the assumed zero lower bound. The level of the cash rate might have become a constraint on policy even in the absence of a big macro shock. That was one of the points I made to the ABE lunch presentation of my pre-pandemic paper on QE back in August 2019.

Changes in the cash rate also move government borrowing costs along the yield curve; impose potential gains and losses on the Bank’s balance sheet (even if they don’t enlarge it); are subject to policy error and potential criticism. You only have to look at recent commentary around the RBA’s latest cash rate cycle to recognise that reputational risk is no less a feature of a cash rate targeting regime and probably a given across different operating frameworks. Yet the AMPT framework views all of these considerations as particular hazards of alternative operating instruments.

It is generally more efficient to conduct policy through a price variable, such as the cash rate or the exchange rate, than a quantity variable. But there are also potentially very large losses in efficiency associated with a framework that treats the effective lower bound as a constraint on policy and that fails to deploy AMPTs in a timely or sufficient aggressive manner. We should be wary of excessively raising the bar to AMPTs when they might be needed.

The RBA’s loss is our gain

The framework states that:

AMPTs that have implications for the balance sheet should be subject to robust internal ex ante financial risk analysis and challenge before they are used, including under severe but plausible adverse scenarios, to ensure the potential consequences are understood and risk accepted. Second, the potential implications for the consolidated public sector balance sheet should be clearly communicated to the Treasury.

The question of where and how any realised losses flowing from a bond purchase program ultimately land on the public sector’s balance sheet is a second-order issue. Any cost to the RBA as a holder of government bonds is a corresponding benefit to the government as the issuer of those bonds (although purchases of semi-government securities might result in a transfer between the Commonwealth and the states). Purchases of non-government securities are more problematic from this perspective, although that is not necessarily an argument against them. To the extent that the broader public sector balance sheet suffers realised losses, that is a measure of the interest rate risk that BPP has removed from the private sector. That risk transfer is not an unfortunate side-effect of QE; it is one of the channels through which QE is meant to work.

Monetary policy can be implemented perfectly well by a central bank with negative equity, as has been the case recently, and the balance sheet should not be viewed as a constraint on policy. The fact that a central bank’s balance sheet is denominated in its own irredeemable monetary liabilities is its most distinctive feature and what makes monetary policy such a powerful policy instrument. It is actually a large part of the reason for having a central bank in the first place. While it is important to have a well-capitalised central bank for reasons of budgetary independence from government, central bank capital should not be viewed as a constraint on the use of AMPTs.

The new AMPT framework maintains that BPP has small and uncertain effects on aggregate demand, but also that BPP exposes the Bank to signficiant losses. But we would only expect the latter to arise in situations where a BPP had successfully reflated the economy, which was the pandemic experience. The framework does acknowledge that stronger activity ‘supports tax revenues’ and can ‘strengthen the consolidated balance sheet for a time,’ but it treats these dynamic offsets as something of a footnote. The balance sheet implications of BPP should be viewed as very much a second-order consideration relative to the positive macroeconomic and fiscal effects of a successful reflation.

Reputational risk

Among the key questions the framework directs staff to ask of any tool is:

How might the tool impact the RBA’s reputation or credibility, including the ability to use the tool again in the future?

The largest reputational risk a central bank faces is not that it makes accounting losses on its bond portfolio, or that a policy commitment is overtaken by better-than-expected outcomes. It is that it fails to stabilise the macroeconomy because of self-imposed constraints and an unwillingness to use AMPTs in support of its mandated objectives.

Between March and November 2020, the RBA told us it had already done as much as it could based on an effective lower bound that wasn’t (yet) a binding constraint. We know it wasn’t because the RBA subsequently further lowered the official cash rate and also delivered more stimulus via a BPP. After its April 2020 Board meeting, when policy was left unchanged, the RBA said ‘the Board wishes the best to all Australians as our country deals with this very difficult situation.’ The Board’s best wishes were a poor substitute for the policy support it had withheld.

There is also reputational risk in hiding behind self-imposed technical and operational constraints when the government has given the RBA almost unlimited statutory authority to achieve its delegated policy objectives. Admittedly, this view is based on my somewhat contrarian reading of pandemic era monetary policy. The actual reputational risks played out differently, but that reflects a flawed narrative in relation to the pandemic episode. The new AMPT framework should have been viewed as an opportunity to overturn, rather than buy into, that mistaken narrative.

Risk appetite

The framework’s risk-management section also instructs that:

the MPB will have regard to the GB’s risk appetite, without preventing or impairing the implementation of decisions that are necessary to achieve its objectives. This includes considering options and potential mitigants that can achieve the MPB’s objectives at lower risk.

The saving clause, ‘without preventing or impairing,’ is doing some heavy lifting here and the framework is careful to affirm the MPB’s autonomy. But the practical effect of requiring the MPB to ‘have regard to’ the GB’s risk appetite is to invite the MPB to second-guess the new GB’s risk tolerance before it acts when the historical record shows that the former Board’s risk tolerance was in fact far too low.

The GB is subordinate to the MPB for monetary policy purposes for good reason. A process that nonetheless routes monetary policy decisions through the GB’s risk appetite and asks the MPB to prefer ‘lower risk’ options, is a mechanism by which the Bank might pull its punches in a crisis. The MPB should not have to look over its shoulder at what the Governance Board thinks about balance sheet and other risks when it sets monetary policy.

Big in Japan

The framework’s scenario analysis explicitly contemplates a ‘slow grind down’ scenario: ‘Persistently low demand and inflation due to entrenched low inflation expectations’, expressly modelled on Japan’s experience. It assesses bond purchase programs as only ‘low-medium’ suitability for this case, on the ground that they carry ‘substantial financial risk, particularly if the policy is in place for a prolonged period’.

But this scenario runs directly counter to the recent Japanese experience. Since 2013, Japan is an example of a highly successful reflation achieved through a combination of large-scale asset purchases and yield targeting. The fact that Japan’s cash rate has just risen to its highest level in 35 years and long-term inflation expectations are now consistent with the BoJ’s inflation target for the first time in decades is symptomatic of a successful, monetary policy-led reflation via AMPTs in response to what had been the slowest of ‘slow grind’ scenarios.

Interest rates and term lending facilities

Across all four macroeconomic scenarios, term lending facilities are ranked ‘high’ or ‘medium’. The pandemic experience with the Term Funding Facility was more equivocal than this ranking implies. There was little pass-through of the facility to the existing stock of mortgages (mine in particular!), as opposed to new borrowers, and the framework’s own assessment concedes the facility ‘provided no flexibility on the amount of stimulus’ and ‘introduced interest rate risk.’

The consistently favourable ranking of term lending facilities in the framework’s scenario analysis reflects its underlying preoccupation with interest rates, specifically bank funding costs and their flow-through to lending rates, as the primary transmission mechanism for monetary policy and at the expense of other channels such as the exchange rate.

Exit before you enter

The framework asks that exit strategies be considered ‘from the outset’ and that staff ‘detail options for how tools could be exited’ as part of the initial design. It also recognises the trade-off: ‘stronger commitments can make a tool more powerful, but they also make it harder to exit’, and it acknowledges that signalling the terms of an early exit can undercut a tool’s effectiveness.

That acknowledgement sits uneasily with the requirement to specify the exit strategy up front. The RBA now makes a virtue out of not offering forward guidance in relation to future changes in the cash rate, but the framework suggests a different standard is to be applied to the use AMPTs. The risk created by this element of the framework is of an early exit driven by upfront commitments rather than macroeconomic conditions.

Open-economy crowding out

Kent’s speech notes that bond purchases ‘could also put downward pressure on the Australian dollar…but the extent of this is uncertain and depends in part on the policies of other central banks.’ The RBA’s resort to BPP from November 2020 explicitly recognised that relative monetary conditions in Australia had tightened because other central banks had done more to expand their balance sheets.

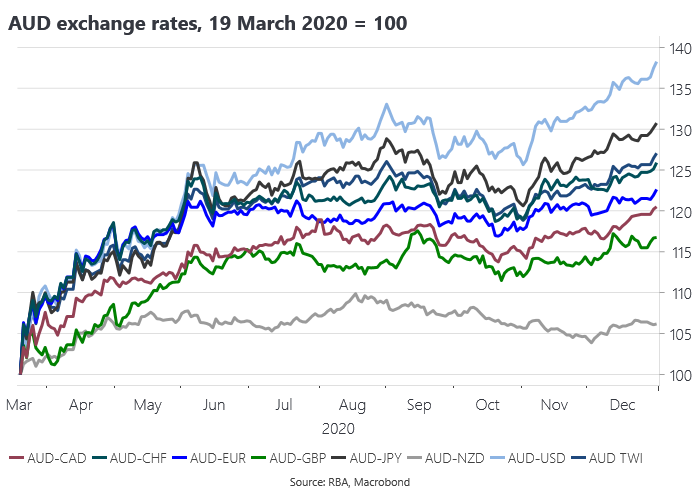

That left Australia with a sub-optimal macro policy mix for a small open economy, one that leaned too heavily on fiscal policy, yielding open-economy crowding-out effects through the exchange rate and net exports. The Australian dollar appreciated broadly against its G10 peers over that period, and Australian long yields sat at the top of the AAA-rated sovereign credit space.

In a small open economy with a floating exchange rate, relative fiscal expansion is offset by an exchange rate appreciation, but relative monetary expansion is amplified by a depreciation. The exchange rate effect of BPP is not merely ‘uncertain’; a failure to deploy it in a timely way, and on a scale comparable to peer central banks, reliably induces an unhelpful appreciation. The dependence on ‘the policies of other central banks’ is an argument for doing more, not less. The framework has not internalised the very obvious lessons from the pandemic experience, even though they were fully conceded by the RBA at the time.

Yield curve targeting

Kent’s account of the yield curve target’s limitations is accurate as far as it goes. A yield target ‘is not well suited to a highly uncertain environment’, shares the challenges of forward guidance, carries ‘material risks to the balance sheet’ and poses risks to market functioning ‘if the exit is disorderly’. All this was understood before the pandemic. But yield curve targeting was chosen anyway as a way of doing easing on the cheap: an attempt to substitute the expected duration of low rates for their magnitude, avoid a large balance sheet expansion, while remaining within the Bank’s traditional operating framework.

It did not avoid a balance sheet expansion. It delayed it, and the delay produced an even larger catch-up program and larger losses than a timelier BPP would have entailed. Yield curve targeting is inherently pro-cyclical: defending the target requires the heaviest purchases at exactly the moment the market is signalling that the stance of policy has become inappropriate. The early exit from yield curve targeting was a symptom of policy success, not failure, yet is now mistakenly viewed as a reputational loss.

Conclusion

The AMPT framework effectively concedes many of my real time criticisms of pre-pandemic and pandemic era monetary policy and yet still manages to avoid internalising many of the more obvious lessons. Kent concludes that the framework ‘puts us in a stronger position to respond in the rare circumstances when the cash rate is very low and additional support may be needed’. In a narrow, sense that is true: the Bank has now thought much more carefully about design, calibration, communication and exit, and who decides what. The RBA is now better placed to fight the last war, just as the world enters a period of secular increase in equilibrium interest rates.

Like the RBA Review before it, the framework is conditioned on a dominant but false narrative around the pandemic episode. Between March and November 2020, the RBA did too little based on self-imposed technical and operating constraints. Its subsequent actions concede as much. But the bigger constraint was intellectual and conceptual: the unwillingness to contemplate the more aggressive use of AMPTs.

Even after the pandemic, following the successful reflation of the economy and the restoration of full employment, Governors Lowe and Bullock largely dismissed the effectiveness of AMPTs. That aggregate demand subsequently overshot was not the worst problem to have and one that ‘conventional’ monetary policy is well equipped to address. If AMPTs were ineffective or unimportant, the RBA would not have had a post-pandemic inflation problem. The counterfactual in which the RBA maintained its yield target for three years would have been a much worse outcome, not just for the macroeconomy, but also the public sector’s balance sheet and, just possibly, the RBA’s reputation. Unfortunately, the conventional narrative around pandemic era monetary policy has all of this exactly backwards. The AMPT framework review is a missed opportunity to push back and re-write that narrative.

ICYMI

Live LLM rankings based on benchmarks and real data from millions of people using models through OpenRouter.

Small-Area Global Elections (SAGE) Dataset by Noah Dasanaike.