US September CPI and Australia’s Q3 trimmed mean inflation rate

Plus, Big Mac steps up his criticisms of the RBA review

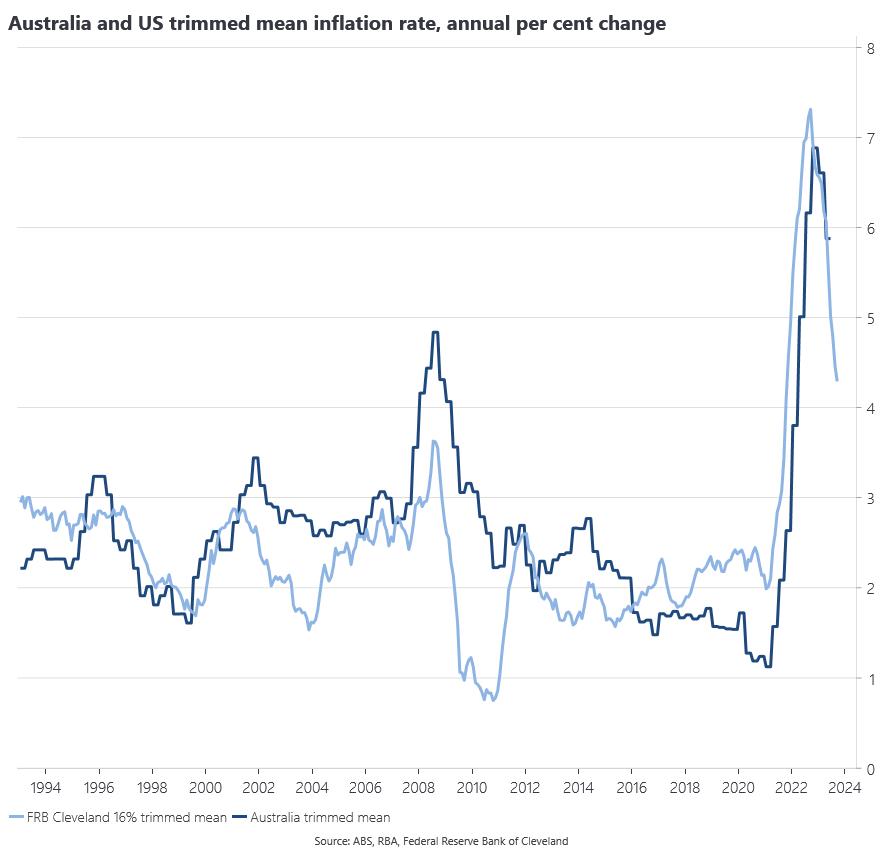

The US September CPI came in a little hotter than expected with a 0.4% increase over the month, leaving the annual rate steady at 3.7%. The core series was steady on the month at 0.3% and moderated over the year to 4.1%.

Excluding shelter costs, the headline CPI is up only 2.0% over the year, which is below the Fed’s 2% target on a PCE basis (US CPI tends to run a bit stronger relative to PCE). While I am not a fan of excluding CPI components without an economic motivation, in the case of housing, there are well-known lags with which house prices and rents enter the CPI and those costs have moderated substantially, which will eventually be reflected in the headline measure.

In the wake of the CPI, sentiment for a further Fed tightening before year-end remains evenly divided. Many financial market participants have been hanging their hat on higher bond yields to keep the Fed steady, pointing to the implied tightening in financial conditions. But as maintained here previously, long bond yields are more likely to reflect expectations for future nominal income growth and so if anything imply a need for further tightening. The Atlanta Fed is nowcasting US Q3 GDP at 5.1%:

The Cleveland Fed’s trimmed mean inflation rate rose 0.4% in September and 4.3% over the year, a moderation on the 4.5% y/y pace seen in August. Based on the Q3 readings, we would still expect Australia’s Q3 trimmed mean to come in at 0.9% over the quarter and 4.8% over the year, down from the 5.9% pace seen in Q2. That gets us slightly more than half-way to the RBA’s August Statement on Monetary Policy forecast of 3.9% for the year-ended in December and so remains very much in line with the RBA’s expectations.