Why is the Australian dollar so weak?

Because the US dollar is now a commodity currency

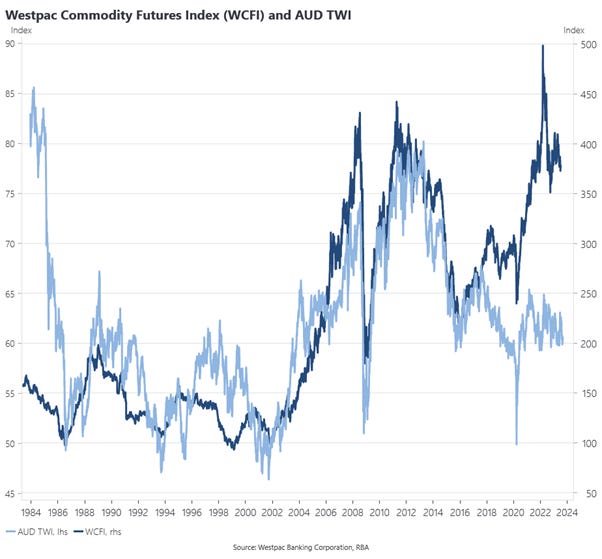

Jacob Greber had a piece in the AFR lamenting the weakness in the Australian dollar, which as many observers have noted, has seen very little benefit from high commodity prices and a terms of trade at record levels, exceeding those seen during the last terms of trade boom in the early 2010s. In fact, this disconnect has been evident since about 2018.

Jake laments the decline in Australia’s international purchasing power, suggests that this is the product of a ‘weak dollar strategy’ between 2014 and 2022 and argues that a weak currency will complicate the RBA’s conduct of monetary policy.

What I think Jake’s analysis misses is that this weakness is not really about the Australian dollar at all. As Daniel Rees notes in a BIS paper from earlier this year, this is really about a change in the relationship between the US dollar and commodity prices. In particular, the US dollar now trades like a commodity currency thanks to the shift in US net oil exports. This has huge implications for the rest of the world, not least Australia. Australia has lost some of the traditional shock absorption role of its exchange rate and this explains why the Australian dollar is no longer responding to the terms of trade as it did during the 2000s and much of the 2010s.

As Rees shows, the US dollar has always behaved like a commodity currency in that there is a strong relationship between the US dollar and its terms of trade. Indeed, on Rees’ estimates, the relationship for the US is even stronger than it is for Australia. But when the US was a bigger commodity importer, a rise in commodity prices was associated with a deterioration in its terms of trade. Now that the US is a big net oil exporter, higher commodity prices are associated with a stronger terms of trade and this is reflected in its exchange rate. As Rees notes, the share of commodities in US exports increased by more than 10 percentage points between 2000 and 2022. The US became a net oil exporter in 2019 and this lines up very nicely with the disconnect between the AUD TWI and commodity prices shown above.

The obvious implication is that if there is a stronger positive relationship between commodity prices and the US dollar, then the traditionally strong association between the USD exchange rate of commodity exporting countries and commodity prices will be weaker, which is exactly what we have seen with the Australian dollar.

It also means that Australia will lose some of the shock absorbing role of its floating exchange rate. When the terms of trade boom, AUD appreciation traditionally moderates the increase in Australian dollar incomes from commodity exports. On the import side, the relationship between the Australian dollar and commodity prices also moderates the effect of oil price shocks, one of the few commodities for which Australia is a net importer. Australia now faces greater volatility in commodity prices in its own currency, not least oil.

This changed relationship has another major implication, which Jake probably won’t like. Australian monetary policy via the official cash rate will now have to become much more activist in order to compensate for the reduced shock absorbing role of the exchange rate. This means easing even more aggressively during global downturns, but will also require tighter monetary policy during global upswings, as Jake notes in his piece. The RBA is going to have to work harder in future.

For Australian investors, the Australian dollar exchange rate may now provide less of a natural hedge for allocations to offshore equities. Traditionally, global cyclical downturns that have weighed on global stocks have seen an offsetting benefit whereby weaker commodity prices have raised the AUD value of offshore equities via a weaker exchange rate. This was an argument for leaving allocations to foreign equities unhedged, avoiding hedging costs. But the value of that natural hedge may now be diminished.

An obvious question to ask is whether the US will continue to be a major net oil exporter. You could argue that the global energy transition will weigh on future US oil exports in an absolute sense, although the US is likely to maintain its position as an oil exporter in relative terms, which is what matters for exchange rates. But it is also worth contemplating the implications of a Trump win in 2024, which will likely lead to a gutting of US government efforts on climate change. Trump would have few compunctions about presiding over the US as a petro-state.

The US dollar now trades more like the Australian dollar used to. Benchmarking the AUD against its former relationship with the commodity prices is likely to be misleading. AUD valuation models need to be updated accordingly.

ICYMI

Why Canada underperforms its potential (not just Canada).

PropTrack’s new housing affordability index shows the extent of middle class immiseration due to the over-regulation and taxation of Australian housing supply.

Stephen, what do you make of the lacklustre performance of the AUD against other (non-commodity) currencies in recent years, like the Euro? The AUD/EUR was relatively strong in 2022, but is now down below pre-pandemic levels despite commodity prices in your chart remaining well above pre-pandemic levels.