2024 Year in Review: the centre did not hold

Plus, semi-annual sale: 20% off a paid sub forever

2024 ended on a positive note in Australia at least with the passage of the RBA Reform bill, completing the implementation of the most important of the RBA Review recommendations. The Review and the government response was a good example of the posting-to-policy pipeline, in which this newsletter played a small part. While the pre-history of the newsletter dates back to 2003, the Substack version has its origin story in its contrarian, market monetarist-inspired critique of pre-pandemic and pandemic era monetary policy.

It is unfortunate that the bill did not secure bipartisan support. This was partly the result of the compressed timeframe for the Review process and the Review panel not doing enough of the groundwork to secure support for some of its recommendations. The recommendations around section 11 of the RBA Act were barely discussed during the review process. It didn’t come up in my meeting with the Review secretariat and if it had I would have given them a very different perspective to the argument found in the final report.

With the review panel made up of one offshore participant and a senior public servant, it was left to the academic member of the panel to carry the burden of promoting and defending the Review’s recommendations against a concerted and organised campaign against the reforms by the jilted RBA old guard. That was unfair on her but highlights the importance of ensuring that reviews of this type have someone available to back in the recommendations when they are challenged. As it happens, Renee was this week appointed to the new Monetary Policy Board, so she gets to put her recommendations into action.

A key lesson from the review is that any reform process needs to start early in a government’s term. The review was announced in July 2022, even though Treasury began the process of standing up the review before the change of government. The panel did not report until March 2023, the final report and government response was released in April 2023 and the implementing legislation has only just been passed by the parliament. The bill only got up at the last minute as part of package of guillotined legislation. While we will take the win, it was all a little too close to comfort.

My Straussian reading of the RBA Review final report was that it pointed to institutional failure well beyond the RBA and those institutions tried very hard to fail again. As Tom Dusevic observed:

if we can’t do a basic institutional refresh, how will we ever manage to again cut through with disruptive reforms that benefit the quiet many at the expense of the noisy few?

Much of the commentary around the new Monetary Policy Board suggested that its creation placed an extra burden on the Treasurer to appoint qualified people. But that burden has always been there and the new structure doesn’t change that. Former Governor Ian Macfarlane complained in relation to the proposed Monetary Policy Board that ‘we don’t know who they will be’ but that was no more or less true under the existing arrangements. The intent of the RBA Review was to improve the expertise of the Board relative to its own past and the task at hand, which ultimately comes down to the appointment process. That process will still be heavily over-sighted by the official family, in line with the Review’s recommendations.

Prasanna Gai’s paper for the RBA Review laid out in devastating detail the existing Board’s shortcomings. Prasanna and I are both former students of the most qualified of the existing non-executive Board members but we both argued that the existing Board arrangements were unsatisfactory and needed to change. Prasanna and I put up a model somewhat different to that recommended by the Review. There is no unique way of doing it, but most of the proposed models were improvements on the status quo. The new Monetary Policy Board will be up and running on 1 March 2025 and Treasurer Chalmers announced the new appointments to the Monetary Policy and Governance Boards this week.

The appointments to the Monetary Policy and Governance Boards have been very well received. Having previously worked or studied with several of the appointees, I can vouch for the fact the RBA is in good hands.

The centre did not hold

I spent much of the year highlighting the implications of a second Trump administration, reflecting his steady ascent in the prediction market betting odds. We did Trump the favour of taking his ideas seriously and now we will all have to live through them. I won’t rehearse that discussion here, but pop Trump into the search bar if you want to re-visit those posts.

We paid close attention to prediction markets as a guide to the election outcome. Despite the numerous regulatory barriers put in their way, these markets performed the classic Haykeian function of revealing tacit and distributed knowledge. As we argued during the election, the presence of noise traders arguably makes prediction markets more efficient, not less. Note efficiency in this context does not mean getting the election result right ex post, but drawing upon a larger information set than used by pollsters and poll-based election models ex ante.

I landed at USSC in 2018 just in time for Trump’s first trade war, which made that job very easy, at least initially. Later in my time at USSC I had it relayed to me that, as a free trader, maybe I was no longer the right person in that role because the ‘world had moved on.’ But the laws of economics continue to hold, whether the world chooses to believe in them or not. In his 1970 book Power and Money: The Economics of International Politics and the Politics of International Economics, Charles Kindleberger wrote that:

The economist's role is to argue for the general interest, for cosmopolitanism, and for an open system that benefits the world at large, even if it is often at odds with narrower, parochial, and nationalist interests.

That motivation will continue to inform this newsletter as we go into the new trade wars of 2025.

Markets in 2024

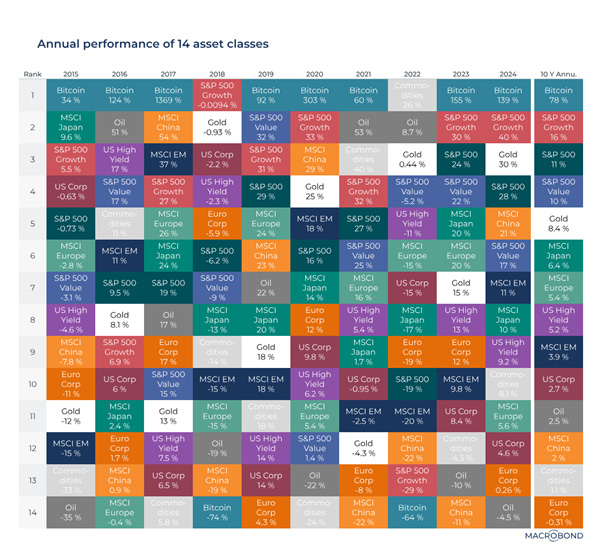

MB produced this handy summary of asset markets returns in 2024 and for the last 10 years. In each of the last 10 years, BTC has been either at the top or bottom of the league table, a fact that tells you most of what you need to know about BTC. BTC made new record highs this year and outperformed S&P 500 growth stocks in both 2023 and 2024.

That performance only serves to highlight BTC’s high beta to risk assets. One of the newsletter’s themes this year has been that supposed safe havens like BTC and gold (which came at 3rd place in 2024) have behaved much like stocks, which means they are not really safe havens. At the risk of stating the obvious, such a high beta means that in context of a 10-20% equity market drawdown, you should expect BTC to be down even more. Your boring S&P 500 index fund came in 4th in 2024 and 3rd on average over 10 years. Buy the index and you might have some bad years in an absolute sense, but you won’t do terribly in a relative sense.

China stocks went from worst performer in 2023 to 5th, partly due to some heavy-handed guidance from the CCP to local institutions to buy. China MSCI returned 2% on average over the last decade, validating our longstanding bearishness on the Chinese economy. Not shown in the table, but China’s 10-year bond made record lows in yield and ultra-long duration bond yields fell below those in Japan, which tells you most of what you need to know about China’s growth prospects. Foreign institutions were having none of it, with heavy net foreign portfolio and direct investment outflows. Invoking fiscal stimulus as the solution to China’s problems was perhaps the laziest of the sell-side narratives, allowing analysts to wave away China’s structural problems. The value contrarians declared China a buy, but the absolute and relative valuations were all too consistent with the fundamentals.

Hedge fund returns tell a similar story, with fundamental equity growth funds topping the HFR hedge fund indices YTD, but underperforming your S&P 500 index fund. Discretionary and systematic macro struggled to beat cash. Macro arbitrage is a tough business. Just ask Scott Bessent. But fear not, the 2025 economic lollapalooza is nearly here.

The hedge fund sector returned 5.8% YTD. No one really buys the whole sector, although some fund-of-funds might approximate the index and pod shops will often straddle multiple hedge fund styles. The danger with these exposures is that the alpha they generate cancels out and you are just left with the deadweight loss of asset management fees.

US equities have had an exceptional run, which left the usual suspects flailing about looking for reasons why it might all come to an end, as if Trump’s election were not a good enough reason. Ruchir Scharma ludicrously suggested that Trump’s tariffs would make China stimulate its economy, making China look better on a relative basis. Sure.

Ultimately, US outperformance is a function of its institutions and those institutions are under threat like never before. Some of the people most opposed to Trump are those with the strongest belief in American exceptionalism. I said earlier in the year US dollar assets could still be expected to outperform under Trump, but largely due to negative spillovers from US policy to the rest of the world. Whether it is Germany, France or South Korea, politics and policy doesn’t look a whole lot better elsewhere, which keeps the US looking good on a relative basis. But Trump could do a lot of damage in absolute terms.

The newsletter in 2024 and semi-annual sale

Growth was more subdued this year, with total subscribers up 22% compared to the end of 2023. Subscriber acquisition is mainly driven by reader shout-outs along with good old fashioned Google search, which was surprisingly the number one source of paid subscribers this year. Substack must be doing a good job on SEO. Thank you to everyone who plugged the newsletter on various platforms.

Substack is essentially enterprise software that allows a direct relationship with readers un-intermediated by an algo-driven platform or other gatekeepers. Substack also has an app-based platform and network, but most of you consume this newsletter via email or RSS (a reminder that the Substack url also serves as an RSS feed).

I don’t market the newsletter or annoy readers with repeated subscription offers or requests to subscribe. Nagging you is not going to make you want it more (and quite possibly less). I do two sales a year, one for the end of the June financial year and one for year-end. So here it is: take out a paid subscription between now and 1 January and receive 20% off the subscription price forever.

By taking out a paid subscription, you not only help cover the cost of the many inputs that go into the newsletter, but also support its mission to promote better public policy.

There is a standing 50% discount for email addresses affiliated with educational institutions (pro-tip: alumni email addresses seem to work with this).

For existing paid subscribers, I have tried to return the favour by linking back to your newsletters and other work where relevant to this readership, including in the ICYMI section. I am happy to exchange recommendations with other newsletters using Substack’s powerful recommendations feature. Also open to making complimentary paid subscriptions available on a reciprocal basis to other newsletter writers.

Group subscriptions are easy to organise amongst yourselves and are subject to a discount of 25% per seat with only a two seat minimum. I can arange institutional deals based on domain names. Substack also facilitates gift subscriptions (imagine their surprise!) The Substack algo may also upsell you from time to time.

End of sales pitch. I will be taking a break over the Christmas-New Year period, back in early 2025. Good luck out there.

Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world.